TL;DR. A single invoice from fund counsel can carry 40 to 100 time entries across several legal matters, spanning multiple funds, the GP, co-invest vehicles, and the management company. The hard part is not the math. It is reading each line, deciding which entity actually benefited, choosing a methodology the LPA supports, and leaving a rationale that holds up years later. This is the five-step workflow controllers actually run, with a worked example and the journal entries at the end.

A law firm bills by attorney time, not by accounting bucket. So a $118,500 invoice from fund counsel arrives as a list of narratives like "review transaction documents and confer with client regarding structure," and a controller has to turn that into a defensible split across five or six entities. In Ceviche's analysis of 42 PE and VC firms evaluated between 2025 and 2026, 20 of 42 named legal invoice allocation their single most complex allocation problem, and 35 of 42 were still doing it in spreadsheets.

Legal invoice allocation is the process of splitting one outside-counsel invoice, often with many time-entry lines across several legal matters, across the fund entities, the general partner, and the management company that benefited from the work, using a defined methodology per line and posting the result as audit-ready journal entries.

The pages that rank for this question today do not answer it. A Big Four guide covers GAAP carve-outs for SEC filers. An e-billing tool documents which button splits a line. Two compliance whitepapers tell you to "document your methodology" without ever showing one. None of them sit in the controller's seat with a real invoice. Here is what that work looks like.

Why are legal invoices the hardest allocation problem?

Most fund expenses arrive pre-sorted. A fund administrator's invoice is a fund expense. A SaaS subscription for the deal team is a management company expense. Legal is different, for three reasons.

First, one invoice mixes benefit. A typical messy bill from fund counsel might cover Fund IV formation matters, portfolio acquisition support, side letter negotiations with prospective LPs, regulatory advice for the adviser, GP restructuring, and tax structuring for a co-invest vehicle, all on the same engagement. Some of that belongs to the funds. Some belongs to the adviser. Telling them apart is the job.

Second, the narratives are vague on purpose. Lawyers write for the privilege log, not the general ledger. "Confer with client regarding structure" could mean fund-level deal work or adviser-level fundraising. The controller has to interpret intent, sometimes with follow-up to legal, the deal team, or compliance before anything posts.

Third, the stakes are asymmetric. Nearly every SEC enforcement action on fund expenses turned on the same fact pattern: an expense that benefited the adviser, charged to the funds. The SEC's Division of Examinations has named fee and expense allocation a recurring priority for private fund advisers. Get a legal split wrong in the adviser's favor and the cost is rarely the dollar amount. It is the restatement, the LP question, and the weeks spent reconstructing support during an exam.

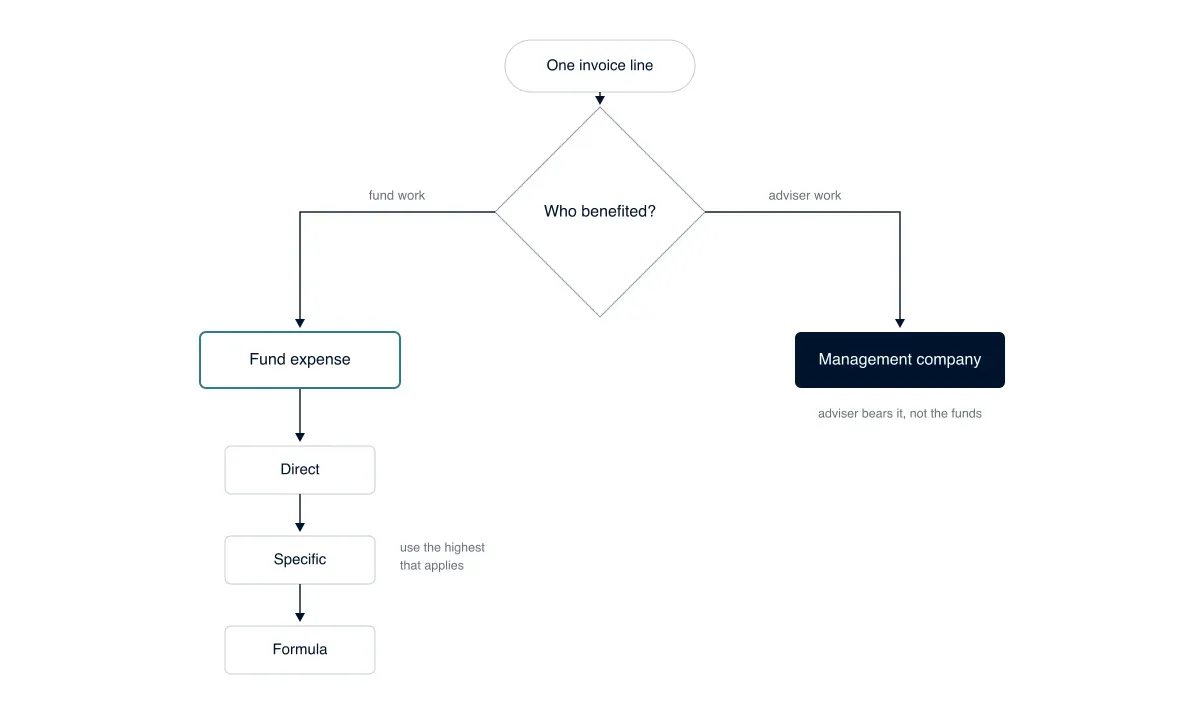

Step 1: Classify each line as fund or management company

The first decision on every line is not "who received the invoice." It is "who benefited from the work, and what do the governing documents permit."

For each line, three questions settle most of it:

- Is the expense expressly chargeable to the fund under the LPA, PPM, side letters, or expense allocation policy?

- Was the work performed primarily for a specific fund investment, fund operation, or fund investor?

- Was the work performed for the adviser business itself: compliance, marketing, fundraising, personnel, or management company operations?

Fund expense vs management company expense. A fund expense is a cost the LPA permits the fund to bear because the work benefited the fund, its investments, or its investors. A management company expense is a cost of running the adviser's business, which the adviser bears out of its management fee. The split is governed by the fund documents, not by which entity the vendor billed.

In practice the easy lines sort themselves:

| Usually a fund expense | Usually a management company expense |

|---|---|

| Portfolio acquisition diligence | SEC examinations and adviser registration |

| Financing documentation for a fund investment | RIA compliance consulting |

| Portfolio company restructuring | Marketing and fundraising activities |

| Fund-level tax work | Employee compensation matters |

| LP reporting legal review | Management company corporate governance |

| Fund formation costs, where the documents permit |

The judgment lives in the mixed-benefit lines: side letters negotiated with prospective investors, successor-fund fundraising while current funds are still active, adviser-level regulatory work that indirectly helps the funds, shared tax structuring, and GP restructuring that touches several vehicles. Those are exactly the lines an auditor or examiner circles, so they are the ones worth slowing down on.

Step 2: Pick the allocation methodology for each line

Once a line is classified, the methodology follows a hierarchy. Work down it, and only reach for a formula when you have to.

Allocation methodology is the rule used to divide one expense among the entities that benefited from it. The common drivers are direct attribution to a single entity, specific-beneficiary splits among the entities involved, and formula-based allocation by committed capital, invested capital, NAV, ownership percentage, or transaction participation.

Direct attribution comes first. If a line clearly relates to one fund or one investment, charge it there. Legal diligence for a Fund IV portfolio company goes to Fund IV. A side letter for an investor in Fund V goes to Fund V. This is always the preferred method because it needs no defending.

Specific-beneficiary allocation comes second. If several entities benefited, split it among them by the benefit each received. Acquisition financing work on a deal that Fund IV and a co-invest vehicle pursued together gets split by their participation in that deal.

Formula-based allocation is the fallback. When direct attribution is impractical, apply a predefined driver: committed capital, invested capital, NAV, ownership percentage, or transaction participation. Shared tax structuring across parallel funds, for instance, often splits by committed capital.

The LPA usually says less than people expect. It typically says the fund may bear expenses incurred in connection with its investments, operations, tax, reporting, legal, and accounting, and that shared expenses are allocated in a "fair and equitable" manner. What "fair and equitable" means, which driver to use, and how to treat mixed-benefit lines is left to judgment. That gap is why a written policy applied consistently is worth more than any single clever split.

Every line starts with the same question: who benefited from the work.

Step 3: A worked example with real numbers

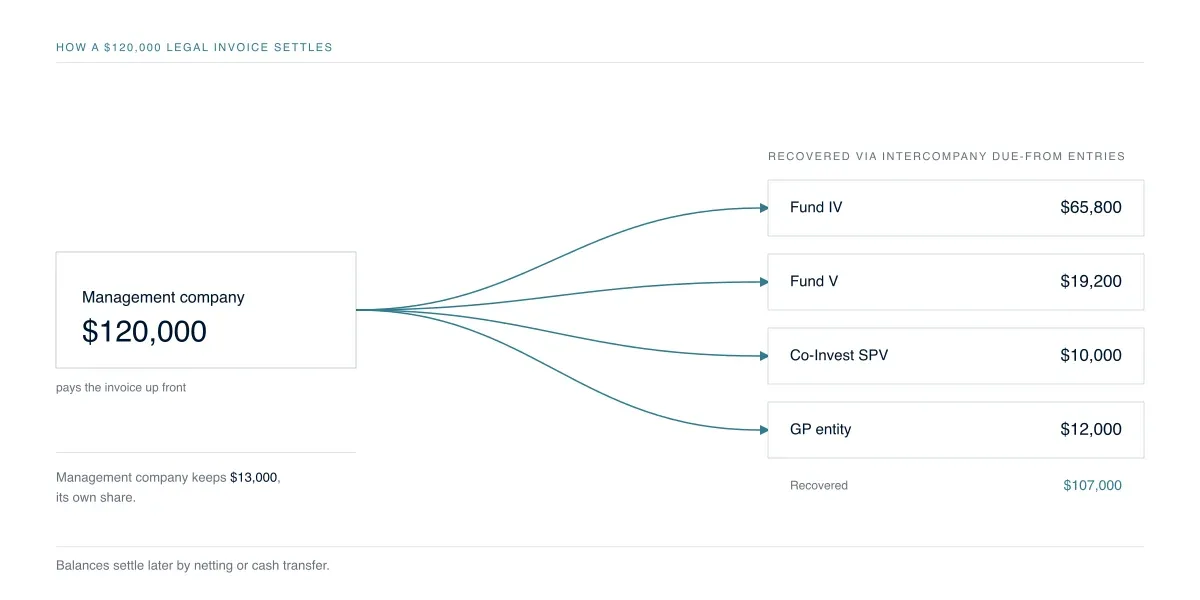

Here is a representative invoice. Fund counsel bills $120,000 across six matters. The fund family is Fund IV (committed capital $300M), Fund V (committed capital $200M), a co-invest SPV that took 50% alongside Fund IV on one deal, the GP entity, and the management company.

| Matter | Amount | Classification | Methodology | Allocation |

|---|---|---|---|---|

| Portfolio acquisition diligence | $45,000 | Fund | Direct attribution | Fund IV $45,000 |

| Co-investment financing docs | $20,000 | Fund | Transaction participation, 50/50 | Fund IV $10,000 · Co-Invest SPV $10,000 |

| Fund V side letter negotiations | $12,000 | Fund | Direct attribution | Fund V $12,000 |

| Parallel-fund tax structuring | $18,000 | Fund | Committed capital, 60/40 | Fund IV $10,800 · Fund V $7,200 |

| Adviser compliance and exam prep | $13,000 | Management company | Direct attribution | Management company $13,000 |

| Successor-fund (Fund VI) fundraising | $12,000 | Adviser | Direct attribution | GP entity $12,000 |

| Total | $120,000 | $120,000 |

Rolled up by entity, the invoice lands like this:

| Entity | Allocation |

|---|---|

| Fund IV | $65,800 |

| Fund V | $19,200 |

| Co-Invest SPV | $10,000 |

| Management company | $13,000 |

| GP entity | $12,000 |

| Total | $120,000 |

Two lines carry the lesson. The parallel-fund tax work splits 60/40 by committed capital, because $300M and $200M of commitments make Fund IV and Fund V 60% and 40% of the combined base. And the Fund VI fundraising line stays off the current funds entirely. Charging successor-fund fundraising to Fund IV and Fund V is one of the most common ways advisers get expenses reclassified after the fact, because that work benefits the adviser raising the next fund, not the investors in the funds already closed.

Step 4: Document the rationale so it survives an audit

The allocation is only half the deliverable. The other half is a record that answers one question years later: why did this line go the way it did.

When an examiner asks "why did this matter go 60/40," a good answer sounds like this:

The invoice related to acquisition financing work supporting a transaction jointly pursued by Fund IV and a co-investment vehicle. We reviewed the legal narratives and allocated by each entity's expected ownership percentage at closing, Fund IV at 60% and the co-invest at 40%. This is consistent with our expense allocation policy and how we have treated similar transactions.

That answer names the beneficiaries, names the methodology, references the policy, and shows consistency. The bad answers are the ones that reveal there is no framework underneath: "that is how we have always done it," "the deal team told us to use 60/40," or "it seemed reasonable."

The single most common mistake is not misallocating an expense. It is failing to document the rationale for a judgment-based split. A close second is charging adviser-related work, fundraising, compliance, or management company governance, to the funds because it feels "fund-related" in a broad sense. Larger managers usually keep a formal expense allocation policy developed with counsel. Smaller managers often run on informal practice that lives in spreadsheets, email chains, and one person's memory, which is exactly what falls apart under examination.

A defensible support file for each allocated invoice holds the original invoice PDF, the allocation worksheet, the LPA references where they apply, the policy citation, the approval evidence, and the journal entry support. Build it as you post, not when the auditor asks.

Step 5: Post the intercompany journal entries

Once the split is set, posting creates intercompany entries because one entity usually pays first. If the management company pays the $120,000 invoice, it carries its own $13,000 and books receivables from each fund and the GP for the rest.

A representative pair of entries, using the co-invest financing line:

Management company books

Debit Legal expense (own share) $13,000

Debit Due from Fund IV $65,800

Debit Due from Fund V $19,200

Debit Due from Co-Invest SPV $10,000

Debit Due from GP entity $12,000

Credit Accounts payable $120,000

Fund IV books

Debit Professional fees $65,800

Credit Due to management company $65,800

The intercompany receivables and payables are then settled periodically through cash transfers or netting. This is where most stacks fall short. AP platforms like Bill.com, AvidXchange, and Stampli are invoice-routing tools, not allocation engines. They move the invoice for approval, but the line-level decision still happens in a worksheet, and the controller posts summarized entries to the GL by hand. The keying is usually done by a fund or senior accountant, reviewed by the controller, and approved by the CFO depending on materiality.

One invoice, paid once by the management company, then recovered from the entities that benefited.

What do controllers get wrong?

Across the firms we work with, the pattern I keep seeing is the same. The expensive errors are never arithmetic. They cluster in a few places. A mixed-benefit line gets a default split with no documented reason behind it. Adviser costs drift onto the funds under a loose reading of "fund-related." Methodology wanders quarter to quarter, so the same kind of work gets allocated one way in March and another way in June. That last one is what examiners catch first, because inconsistency is easier to spot than a single debatable split.

And the cost almost never shows up as the dollar value of the expense. It shows up later: audit scrutiny, a reclassification or a restatement, an LP question the controller has to answer in writing, compliance remediation, and the days lost recreating support for an entry posted two years ago. The teams that stay out of that bucket are not the ones with the cleverest methodologies. They are the ones whose splits are consistent and documented well enough that a stranger could follow the logic.

Where does Ceviche fit?

Most of this workflow is judgment, and judgment stays with the controller. What does not have to stay manual is the part after the decision: applying the methodology consistently, writing the intercompany entries to the general ledger, and assembling the support file as you go.

That is the layer Ceviche automates. Flybridge used to spend a full day each quarter allocating across 18 fund entities in spreadsheets. They now run it hands-off through Ceviche at around 99% accuracy, on top of their existing Bill.com and QuickBooks Online stack, and they onboarded in two weeks. The allocation logic is set once and applied the same way every time, and every posted entry carries its rationale, so the support file is built by the time anyone asks for it. You can see how Ceviche handles fund expense allocation.

FAQ

What does it mean to allocate a legal invoice? It means splitting one outside-counsel invoice across the entities that benefited from the work, the funds, the GP, co-invest vehicles, and the management company, deciding a methodology for each line and posting the result to each entity's general ledger with a documented rationale.

Are legal fees a fund expense or a management company expense? It depends on the line, not the invoice. Work that benefited a fund's investments, operations, or investors is usually a fund expense if the LPA permits it. Adviser work, compliance, fundraising, registration, and management company governance, is usually a management company expense the adviser bears from its fee.

How do PE firms split a legal invoice between funds? They work down a hierarchy: direct attribution to one fund or investment first, specific-beneficiary splits among the entities involved second, and formula-based allocation by committed capital, invested capital, NAV, or transaction participation when direct attribution is impractical.

What are the three methods of cost allocation for funds? Direct attribution charges a line to the single entity that benefited. Specific-beneficiary allocation splits a line among the entities that benefited by the benefit each received. Formula-based allocation applies a predefined driver, most often committed capital, when the first two do not apply.

What does the SEC look for in expense allocation? Whether expenses that benefited the adviser were charged to the funds, whether the methodology is documented and applied consistently, and whether the allocation matches what the fund documents permit. Fee and expense allocation is a standing focus of the SEC's exam program for private fund advisers.

How long does legal invoice allocation take manually? Controllers report spending one to five days per quarter on allocation work, with legal invoices the most time-consuming because each line needs interpretation before it can be split.