TL;DR. Multi-entity accounting keeps a separate ledger for each legal entity in a group, then consolidates them into one set of financials. Shared costs get split across the entities that benefited, intercompany balances get eliminated, and each entity stays auditable on its own. For investment funds, the entities are the management company, the funds, and the SPVs.

What is an entity, and what makes accounting "multi-entity"?

An entity is anything with its own legal identity and its own books: a subsidiary, a division set up as a separate company, a branch, a special-purpose vehicle. The moment a group runs more than one of these, it has a choice. It can throw everything into one ledger and lose the ability to report on each piece, or it can keep a ledger per entity and take on the work of consolidating them. Multi-entity accounting is the second path.

Multi-entity accounting keeps a separate general ledger and chart of accounts for each legal entity in a group, allocates shared costs across the entities that benefited, tracks and eliminates intercompany balances, and consolidates the entities into one set of parent financials while each entity stays auditable on its own.

The defining feature is that nothing lives in just one place. A single insurance premium, a shared office lease, an outside-counsel bill: each one touches several entities and has to be divided, posted, and reconciled across all of them. The arithmetic is simple. Doing it the same way every period, and proving you did, is not.

How does multi-entity accounting work?

Three mechanics carry the whole discipline. Get these right and the rest is bookkeeping.

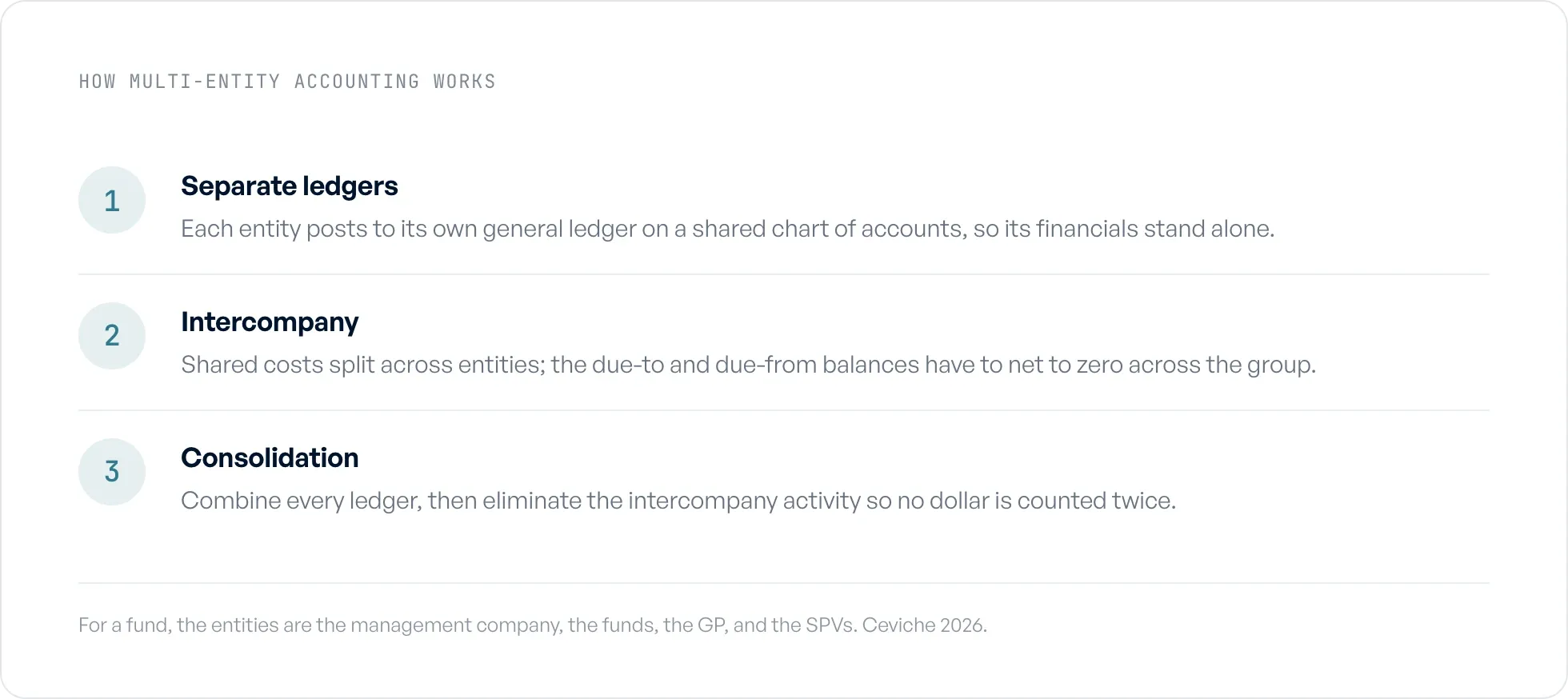

Separate ledgers and a shared chart of accounts. Each entity posts to its own general ledger so its financials stand alone. Most groups run a common chart of accounts across entities so the numbers line up when it is time to combine them. A mismatched chart is the first thing that turns consolidation into a manual cleanup job.

Intercompany transactions. When one entity pays a cost that belongs to another, you record a due-to on one set of books and a due-from on the other. These balances have to net to zero across the group. If the management company fronts a bill that three funds owe, four entities now carry linked entries that all have to agree. For the full mechanics, see intercompany accounting for funds.

Consolidation. To see the group as a whole, you combine every entity's ledger and then strip out the intercompany activity, so a dollar one entity owes another does not show up as both revenue and expense at the parent level. What survives elimination is the real picture.

Currency and jurisdiction add a fourth layer for global groups: multiple currencies to translate and multiple tax regimes (VAT, GST) to honor. For most US private funds this layer is light, since the books are largely in dollars. The harder constraint is the LPA, which dictates what each fund can be charged. That is where the fund version diverges from the textbook one.

How multi-entity accounting works, in three steps.

What is multi-entity accounting for an investment fund?

Here is the part the ERP vendors skip. A fund manager is a multi-entity group, but it does not look like a holding company with tidy subsidiaries under one ERP. It looks like a management company on one general ledger, a set of funds and SPVs on a separate fund-accounting system, and a stack of spend tools feeding both. The entities are real and legally distinct, and they almost never sit in the same system.

Across the 80 PE and VC fund finance teams we spoke with, 96% named multi-entity complexity a core pain, and 92% were running allocations across systems that do not talk to each other. That second number is the fund-specific twist. The textbook assumes one ERP rules everything. In a fund, the management-company GL (usually QuickBooks or NetSuite) and the fund-side system (Investran, AllVue, Carta) are different products, and the allocation has to bridge them by hand.

Scale tells the story. The firms we see most often run from five to thirty-plus entities, and the larger managers run a hundred or more vehicles. A single legal or vendor invoice routinely splits across eight to thirteen funds and SPVs at once. One growth-equity controller described exactly that: one bill, a dozen vehicles, every quarter. At that point "multi-entity accounting" stops being a definition and becomes a Tuesday afternoon with a spreadsheet open and a deadline approaching.

Where does multi-entity complexity actually concentrate?

It concentrates in shared-cost allocation, and specifically in the moment a single cost has to be carved across many entities. This is where the discipline either holds or quietly breaks.

The break is almost always Excel. Of the teams we spoke with, 81% still allocate in Excel: one workbook, rows of invoice lines, columns of entities, percentages someone set three funds ago. It is the real incumbent in this category, far more than any software. It works until the entity count climbs or the person who maintains it leaves, and then the methodology lives nowhere anyone can find it.

Legal invoices are the sharpest version. 63% of teams flagged legal-invoice allocation as one of their hardest splits. A single outside-counsel invoice can carry dozens of timekeeper lines spanning several matters, several funds, the GP, co-invest vehicles, and the management company, and different lines need different methodologies: committed capital for the deal work, a specific fund for formation costs, the management company for anything that benefited the manager. One bill, one PDF, and a dozen judgment calls before a number can be posted.

A worked example: one invoice across three entities

Say outside counsel sends a $40,000 invoice for a deal the firm pursued. The work splits like this:

| Invoice line | Amount | Methodology | Entity |

|---|---|---|---|

| Deal due diligence | $24,000 | Committed capital | Fund II 70%, co-invest SPV 30% |

| Fund formation memo | $10,000 | Specific fund | Fund II 100% |

| General fund counsel retainer | $6,000 | Management company | ManCo 100% |

That single bill produces journal entries in three entities. The deal line splits $16,800 to Fund II and $7,200 to the SPV by committed capital. The formation line books $10,000 to Fund II. The retainer sits with the management company, because the LPA does not let you push general manager overhead to the funds. Multiply this by twenty invoices a month across twenty-six entities and you have the real shape of multi-entity accounting at a fund, which no generalist primer shows you.

What does multi-entity accounting mean for the audit trail?

It means the record has to survive an examiner, not just close the period. Every incumbent primer calls this "compliance risk" and moves on. For a fund, it is concrete: the SEC's Division of Examinations has named fee and expense allocation a recurring priority for private fund advisers, and an exam request can ask you to prove, line by line, that a shared cost was split per the fund documents.

49% of the teams we spoke with had a gap in their audit trail: the allocation happened, but the rationale behind each line did not survive in a form an examiner would accept. The honest test is simple. If an examiner asks how a particular invoice was split eighteen months ago, can you answer in fifteen minutes, or does it take a week and a half of reconstruction? The teams that stay calm during an exam build the support as they post, so every allocated line already carries its methodology, its approver, and its date. Consistent logic applied per the LPA, with audit-ready entries written back to the GL, is the difference between a quiet exam and a fire drill.

What stack do funds actually run for this?

No generalist primer will tell you, because each one only names its own ERP. The reality is that multi-entity accounting at a fund sits across a stack, not inside a single system.

| Management-company GL | Share of teams |

|---|---|

| QuickBooks (Online + Desktop) | 51% |

| NetSuite | 23% |

| Sage Intacct | 5% |

| Everything else (Xero, Quorum, Campfire, Carta, Workday) | 21% |

| Spend / AP tool | Share of teams |

|---|---|

| Ramp | 49% |

| Bill.com | 39% |

| Expensify | 30% |

| Concur | 11% |

QuickBooks and NetSuite alone are the management-company GL for nearly three-quarters of the teams we spoke with, with a separate fund-side system behind them. On the spend side, Ramp, Bill.com, and Expensify carry most of the volume. The allocation has to read from the spend tools, apply the methodology, and post back to the GL. No single product in that list does the cross-system part on its own.

What software handles multi-entity accounting?

For general business groups, ERPs built for this include NetSuite and Sage Intacct, both of which manage separate ledgers, intercompany eliminations, and consolidation inside one platform. That is the right answer when one system genuinely owns all the entities.

It is the wrong answer for most funds, because the management company and the funds already live in different systems and nobody is ripping out a working GL to consolidate them under one ERP. The fund question is not which ERP to standardize on, it is what bridges the manco GL and the fund system you already run. We cover the buying decision in detail in multi-entity accounting software for fund managers, and the broader dataset sits in the state of fund expense allocation.

Where does Ceviche fit?

Ceviche is audit-grade expense-allocation software that sits between the spend systems funds already use (Ramp, Bill.com, Expensify, Concur) and the general ledger (QuickBooks, NetSuite, Sage). It applies the firm's allocation methodologies per the LPA and writes audit-ready journal entries back to the GL with the rationale attached. It is not an ERP and it does not replace your fund-accounting system. Flybridge runs it across 18 fund entities on QuickBooks Online and Bill.com. See how Ceviche handles multi-entity allocation.

FAQ

What is multiple entity accounting? Multiple entity accounting, more commonly written as multi-entity accounting, is keeping a separate ledger and chart of accounts for each legal entity in a group, then consolidating them into one set of financials. Shared costs get allocated across entities, intercompany balances get tracked and eliminated, and each entity stays auditable on its own.

What is the difference between single entity and multiple entity? A single-entity organization keeps one set of books, so every transaction posts to one ledger and reporting is straightforward. A multi-entity organization runs a ledger per legal entity, which adds three jobs: allocating shared costs across entities, recording intercompany due-to and due-from balances, and consolidating the entities while eliminating the intercompany activity.

What is the best accounting software for multi-entity? It depends on whether one system owns all your entities. ERPs such as NetSuite and Sage Intacct handle separate ledgers, eliminations, and consolidation in one platform. Funds whose management company and funds sit on different systems usually need a layer that bridges them rather than a single ERP. We compare the options in multi-entity accounting software for fund managers.

Can an LLC have multiple entities? An LLC is one legal entity, but a group can hold many of them. A management company LLC can sit above several fund LLCs and SPV LLCs, each a separate entity with its own books. That structure is exactly what makes multi-entity accounting necessary: distinct LLCs that share costs and need consolidating.

How do funds allocate a shared invoice across entities? They read the invoice line by line, apply the methodology each line's purpose and the LPA support (committed capital, specific fund, or management company), then post a journal entry to each affected entity and record the rationale. A single bill often produces entries in three or more entities at once.

Why does Excel break for multi-entity funds? The methodology lives in one person's workbook with no audit trail, so it drifts as entities are added and disappears when that person leaves. Of the 80 fund finance teams we spoke with, 81% still allocate in Excel, and it holds up until entity count climbs or an examiner asks how a past split was decided.