TL;DR. Multi-entity accounting software keeps a separate ledger per legal entity and consolidates them, with intercompany eliminations, multi-currency support, and drill-down reporting. For fund managers, the harder job is allocation: splitting one shared cost across the management company, the funds, the GP, and the SPVs, with a different methodology per line. Most multi-entity tools do not do that part.

What is multi-entity accounting software?

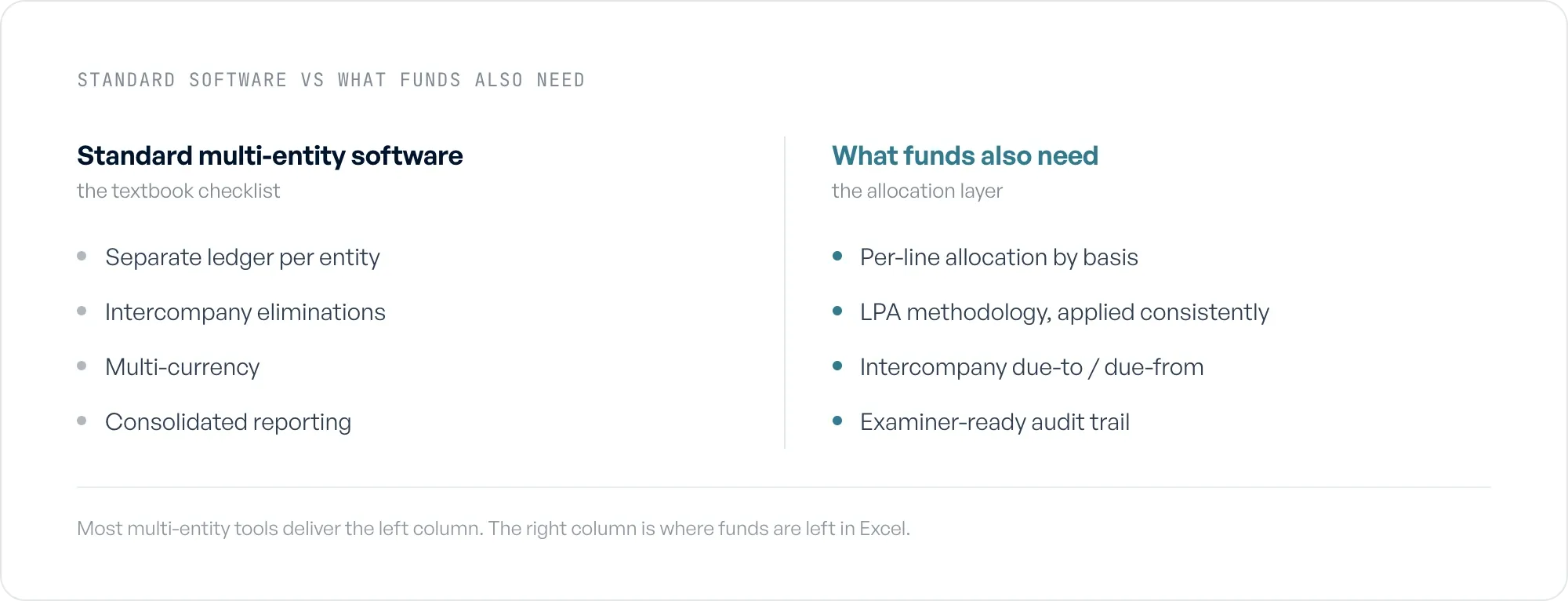

Multi-entity accounting software keeps a separate general ledger and chart of accounts for each legal entity in a group, automates intercompany transactions and eliminations, handles multiple currencies and tax regimes, controls access by role, and consolidates every entity into one set of financials with drill-down to any single entity. That is the textbook definition, and the major platforms all deliver it.

For a fund manager, the word "entities" means something more specific. It means the management company, each fund, the general partner entity, and the co-invest and SPV vehicles, each with its own books and its own rules for what it can be charged. (If you want the underlying mechanics rather than the buying decision, our primer on multi-entity accounting covers ledgers, eliminations, and consolidation in depth.) A holding company allocates shared overhead by headcount or square footage and calls it done. A fund splits a shared cost by committed capital on one line, by a specific fund on the next, and to the management company on a third, because the LPA dictates what each entity carries. The standard software was not built for that distinction.

Most multi-entity tools deliver the left; the allocation layer on the right is the gap.

Why is allocation the real problem, not consolidation?

The buyer's guides frame multi-entity software as a consolidation problem: combine the ledgers, eliminate the intercompany activity, produce one parent statement. Consolidation matters, but it is the easy half. The hard half for a fund is what happens before anything gets consolidated: deciding how one cost gets carved across entities that each have a different claim on it.

This is the most universal pain we found. Across the 80 PE and VC fund finance teams in our research, 96% named multi-entity allocation a core source of complexity, and 92% were running it across systems that do not talk to each other. The typical setup is an expense or AP tool on one side, a general ledger on the other, and a spreadsheet wedged in the middle doing the actual split. Nothing carries the line-level decision from one system to the next, so a person re-keys it, every time, by hand.

Multi-entity allocation is the practice of splitting a shared cost across the fund entities, the general partner, the co-invest vehicles, and the management company that benefited from it, applying a defined methodology to each line and posting the result to each entity's general ledger with a documented rationale. Consolidation rolls those entities up; allocation decides what goes into each one first.

A growth-equity controller we interviewed described single invoices that split across eight to thirteen funds and SPVs at once. The arithmetic was never the problem. Keeping the split consistent, posting it to the right ledger, and proving the logic later, quarter after quarter, is the work. Generic multi-entity software automates the consolidation and leaves the allocation to the spreadsheet.

The features that actually matter for funds

The canonical capability list shows up almost word for word across every page that ranks for this term. Here is that list, with the fund-specific version of each one, because the standard description and the fund reality diverge fast.

Entity-level segmentation and consolidation. Every tool can post to separate ledgers and roll them up. The fund test is whether it can do this when the management company sits on QuickBooks or NetSuite and the funds sit on a separate fund-accounting system. They usually do not share an ERP, so the consolidation that lives inside one platform does not reach across the real divide.

Automated intercompany transactions and eliminations. When the management company fronts a bill that three funds owe, you book a due-from on the manco and a due-to on each fund, and the balances net to zero. Standard tools handle this within their own ledgers. The fund problem is intercompany activity that spans two different systems, which is exactly where the automation stops and the manual entries start.

Multi-currency and multi-tax. Genuinely important for global subsidiaries with mixed currency and VAT or GST exposure. For most US private funds this layer is light, since the books are largely in dollars. The binding constraint is not currency translation, it is the LPA, which governs what each fund can be charged and which no generalist tool encodes.

Role-based access and approval workflows. Table stakes, and funds need them for the same reason anyone does: a controller drafts, a CFO approves, and the system records who did what. The fund-specific add is that the approval has to attach to a specific allocation decision. A signature alone is thin. The record an examiner wants shows how the number was split and on what basis.

Unified dashboards with drill-down reporting. Drill from the consolidated group into one subsidiary, then into one transaction. Useful. For a fund the more valuable drill-down is the reverse: from a single shared invoice down to every entity it touched and the methodology that put each piece where it went. That is the view an examiner asks for, and it is the one the standard reporting layer rarely produces.

The hardest part no tool handles is legal-invoice allocation

This is the sharpest pain in the dataset and the one no competing page mentions. 63% of the fund finance teams we interviewed named legal-invoice allocation one of their hardest problems. A single outside-counsel invoice can carry dozens of timekeeper lines spanning several matters, several funds, the GP, co-invest vehicles, and the management company, and different lines need different methodologies. One bill, one PDF, and a dozen judgment calls before a number can be posted.

Walk through a real one. Outside counsel sends a $48,000 invoice for a deal the firm pursued across two funds and a co-invest vehicle. It splits like this:

| Invoice line | Amount | Methodology | Where it lands |

|---|---|---|---|

| Deal due diligence | $30,000 | Committed capital | Fund III 65%, co-invest SPV 35% |

| Fund III formation work | $12,000 | Specific fund | Fund III 100% |

| General partnership counsel | $6,000 | Management company | ManCo 100% |

That one bill produces journal entries in three entities. The due-diligence line splits $19,500 to Fund III and $10,500 to the SPV by committed capital. The formation line books $12,000 to Fund III. The general counsel retainer sits with the management company, because the LPA does not let you push general manager overhead to the funds. Now multiply it: dozens of these a quarter, each with a different mix of lines and entities. No consolidation engine does this. The methodology lives in the controller's head and the spreadsheet, and the software waits downstream for the answer.

The reason public information is no help here is that "legal invoice software" returns law-firm billing tools, because almost nothing connects splitting a LEDES invoice across fund entities to fund accounting. It is a fund-finance problem wearing a legal-billing costume.

Audit trails and SEC-exam readiness

Every page in this category says "audit-ready" and moves on. For a fund that phrase has to mean something an examiner accepts: the why-each-line-went-where record, attached to the allocation, surviving eighteen months later. 49% of the teams we interviewed had a gap there. The allocation happened, but the rationale behind each line did not persist in a form that holds up under scrutiny.

The stakes are not theoretical. The SEC's Division of Examinations has named fee and expense allocation a recurring priority for private fund advisers, and an exam request can ask you to prove, line by line, that a shared cost was split per the fund documents. The honest test: if an examiner asks how a particular invoice was split last year, can you answer in fifteen minutes, or does it take a week and a half of reconstruction? Teams without a trail described their support as someone writing a paragraph after a meeting. Teams with one build the record as they post, so every allocated line already carries its methodology, its approver, and its date before anyone asks.

This is where the generic "approval workflow" feature and a real audit trail part ways. An approval that records a signature is not the same as a record that reconstructs the split.

Can QuickBooks handle multiple entities? And what do funds actually run?

QuickBooks can hold multiple entities, in the sense that you can run a file per company or use the multi-entity handling in QuickBooks Advanced. What it does not do is allocate one cost across those entities with a different methodology per line and write the result back as clean intercompany entries. That gap is why funds reach for something on top, not why they leave QuickBooks.

And most do not leave. There is no public data on what private funds run their books on, so here is ours. On the general ledger side, QuickBooks (Online and Desktop) is the management-company GL for about half the teams we interviewed, NetSuite is a clear second, and together they cover 73% of the management-company general ledgers we saw. Behind that GL usually sits a separate fund-side system (Investran, AllVue, Carta, Geneva).

| Management-company GL | Share of teams |

|---|---|

| QuickBooks (Online + Desktop) | 51% |

| NetSuite | 23% |

| Sage Intacct | 5% |

| Everything else (Xero, Quorum, Campfire, Carta, Workday) | 21% |

| Spend / AP tool | Share of teams |

|---|---|

| Ramp | 49% |

| Bill.com | 39% |

| Expensify | 30% |

| Concur | 11% |

The honest answer to "what do big companies use instead of QuickBooks" is NetSuite, and for genuinely large or global structures, a full ERP. The honest answer for funds is different: they rarely rip out a working GL. They run QuickBooks or NetSuite for the manco, a fund-accounting system behind it, Ramp or Bill.com for spend, and then they do the allocation in Excel. 81% of the teams we interviewed still allocate in spreadsheets. So the tool a fund is actually shopping for is not a replacement ledger; it is something to retire the workbook sitting in the middle of all of them.

The best multi-entity accounting software in 2026, honestly compared

Here is the comparison every buyer wants, scoped to what each tool genuinely does well, and with one column the other guides leave out: whether it handles fund allocation, the splitting of a shared cost across entities by a different methodology per line.

| Tool | Best fit | Multi-entity consolidation | Intercompany eliminations | Fund allocation (per-line methodology) |

|---|---|---|---|---|

| NetSuite OneWorld | Mid-to-large groups standardizing on one ERP | Strong, in-platform | Yes | Manual; not built for fund-line splits |

| Sage Intacct | Multi-entity finance teams wanting deep dimensions | Strong | Yes | Manual; dimensions help, methodology does not |

| QuickBooks Advanced | Smaller groups outgrowing basic QuickBooks | Limited | Partial | No; allocation stays in Excel |

| Xero | Small multi-entity businesses | Light | Partial | No |

| Dynamics 365 Business Central | Mid-market on the Microsoft stack | Strong | Yes | Manual |

Read the last column honestly. For a general business group where one ERP owns every entity, NetSuite, Sage Intacct, or Dynamics 365 is a sound answer, and the consolidation works as advertised. For a fund, every row reads "manual" or "no" in the column that matters most, because none of these tools was built to split a legal invoice across funds by committed capital on one line and a specific fund on the next. They consolidate what you give them. They do not decide what to give each entity.

A controller we interviewed put the real situation plainly: the accounting systems out there each do a piece of the thing, not the whole thing. That is the buying problem for a fund. The question is not which ERP to standardize on. It is what bridges the manco GL and the fund system you already run and handles the allocation in between. The payoff when that layer exists is measurable: one multi-billion-dollar fund cut its month-end allocation work from roughly 10 days of manual reconciliation to a 1-to-2-hour automated run, taking 5 to 10 days off close. No ERP in the table above publishes a number like that, because allocation is not the job it was built for. See the fund close-time benchmark for the full data.

Where does Ceviche fit?

Ceviche is audit-grade expense-allocation software that sits between the spend systems funds already use (Ramp, Bill.com, Expensify, Concur) and the general ledger (QuickBooks, NetSuite, Sage). It applies the firm's allocation methodologies per the LPA and writes audit-ready journal entries back to the GL with the rationale attached. It is not an ERP and it does not replace your fund-accounting system. Flybridge runs it across 18 fund entities on QuickBooks Online and Bill.com, going from a full day of spreadsheet allocation each quarter to a hands-off run at about 99% accuracy, onboarded in two weeks. See how Ceviche handles fund allocation.

FAQ

What is the best accounting software for multi-entity? It depends on whether one system owns all your entities. For a general business group, ERPs such as NetSuite OneWorld and Sage Intacct handle separate ledgers, intercompany eliminations, and consolidation in one platform. For funds whose management company and funds sit on different systems, the better answer is usually a layer that bridges them and handles allocation, not a single ERP swap.

Can QuickBooks handle multiple entities? Yes, by running a file per company or using QuickBooks Advanced for basic multi-entity handling. What it does not do is allocate one shared cost across those entities by a different methodology per line and write back clean intercompany entries. That is why most funds keep QuickBooks and add an allocation layer rather than migrating off it.

What is multi-entity accounting software? Software that keeps a separate general ledger and chart of accounts for each legal entity, automates intercompany transactions and eliminations, supports multiple currencies and tax regimes, controls access by role, and consolidates every entity into one set of financials with drill-down to any one entity. For funds, the entities are the management company, the funds, the GP, and the SPVs.

What do big companies use instead of QuickBooks? NetSuite is the most common step up, with Sage Intacct and Dynamics 365 Business Central also in the mix, and full ERPs (SAP, Workday) at the largest scale. Funds are a special case: in our 2026 data NetSuite runs about a quarter of management-company ledgers, but most funds keep QuickBooks and add a layer on top rather than replacing the GL.

What is the difference between multi-entity and multi-currency accounting? Multi-entity accounting keeps separate books per legal entity and consolidates them; multi-currency accounting translates transactions and balances across different currencies. They often appear together in global groups, but they solve different problems. A US fund can be deeply multi-entity and barely multi-currency, since its books are mostly in dollars.

Do I need an ERP to manage multiple entities? No. An ERP makes sense when one system can genuinely own every entity. Most funds run the management company on QuickBooks or NetSuite and the funds on a separate fund-accounting system, then layer allocation on top. Ripping that out to consolidate under one ERP is rarely worth it, and it does not solve the allocation problem on its own.

Is multi-entity accounting software only for large companies? No. The trigger is entity count and shared-cost complexity, not size. A sub-$1B fund running three funds, a GP, and a few SPVs already splits costs across six or more sets of books. In our research, fit tracked entity count far better than assets under management.

What should fund managers look for in multi-entity accounting software? Per-line allocation methodology, not just consolidation. Integration with the GL and spend tools you already run rather than a full migration. Intercompany entries that span two systems. And an audit trail that records why each line went where, in a form an examiner accepts. The standard multi-entity checklist covers everything except the allocation, which for a fund is the whole job.