TL;DR. In 2026, 49% of fund finance teams (39 of 80) have a gap in their allocation audit trail: the split happens, but the record of why each line went where it did would not survive an SEC exam. The teams that closed it build the support as they post, so an exam request takes minutes instead of a week and a half.

Key findings

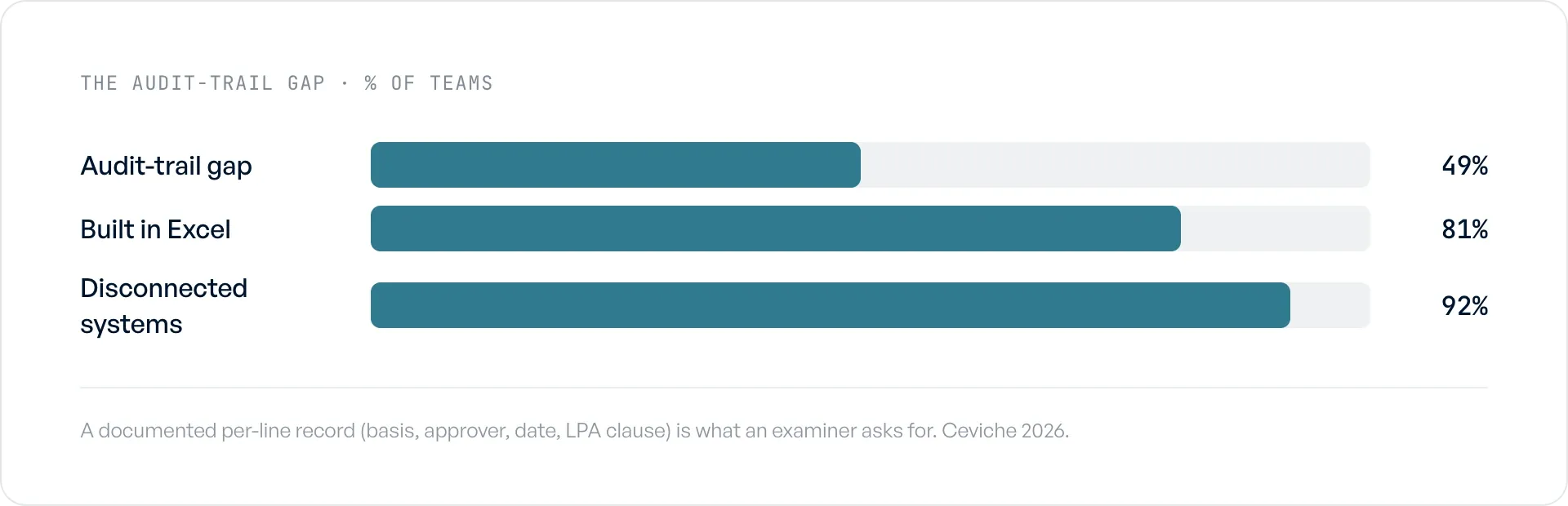

- 49% of fund finance teams (39 of 80) have an allocation audit-trail gap.

- 81% (65 of 80) still allocate in Excel, which leaves no native trail behind the split.

- Teams with a real trail answered an SEC exam request in minutes instead of a week and a half.

Methodology

Based on Ceviche's analysis of 80 PE, VC, growth-equity, and credit fund finance teams interviewed in 2026, coded for the same set of pains, systems, and outcomes.

How common are audit-trail gaps in fund expense allocation?

49% of the teams we interviewed (39 of 80) have a gap in their allocation audit trail. The allocation itself usually gets done. What does not survive is the record of why each line landed where it did, in a form an examiner would accept after the fact. This is the lowest of the five headline pains in our data, and it skews toward the SEC-registered and PE side, which is also where it costs the most.

The reason the rate is this high traces straight to the spreadsheet. 81% of teams (65 of 80) still run allocations in Excel, and a spreadsheet keeps no native trail: it stores the answer, not the reasoning, the approver, or the date. When the methodology lives in one person's tabs and the rationale lives in their head, the trail is only as durable as that person's memory and their file naming.

Closing this requires the audit trail to be built as you post, so every allocated line already carries its methodology, its approver, and its date before anyone goes looking. For the full picture across all five pains, see the state of fund expense allocation.

Where the audit-trail gap comes from, across 80 fund finance teams.

What does the SEC look for in expense allocation?

Fee and expense allocation is a standing focus of the SEC's Division of Examinations for private fund advisers, renewed in its FY2026 examination priorities. In practice, examiners test three things: whether expenses that benefited the adviser got charged to the funds, whether the allocation methodology is documented and applied consistently, and whether each split matches what the fund documents actually permit. Notice that two of the three are about documentation, not about the math.

This is why the gap is quiet. It costs nothing on a normal close, then it costs a lot the moment a letter arrives. A finance lead at a multi-billion-dollar fund put the fear plainly: when the SEC comes in, the team does not think it is doing anything wrong, but proving that is, in their words, "herculean." The exposure is not the allocation. It is being unable to reconstruct it on demand.

What an examiner is really asking for is a per-line record: the basis used, who approved it, the date, and the LPA clause that allows it. Building that as journal entries written back to the GL, rather than reassembling it from email and old spreadsheets, is the difference between a calm response and a fire drill.

What does a thin trail actually look like when the SEC calls?

The teams without a trail described the support for past allocations the same way, over and over: somebody writes it up after the fact. A controller at one fund admitted that the audit record for a quarter's expenses was "just somebody writes a paragraph after the meeting that says we walked through all the expenses and they were all approved." A paragraph is not a methodology, and it is not per-line, so it does not answer the question an examiner is actually asking. The downside is not hypothetical: the SEC has charged private fund advisers over their fee and expense practices.

The contrast in the data is sharp. A finance leader who had been through this at a prior firm watched a real SEC exam request go two ways: handled through a system that produced the record in roughly 15 minutes, versus a week and a half of manual reconstruction the old way. Same request, same firm, two orders of magnitude apart in effort, and the only variable was whether the trail existed before the request came in.

That gap closes when the trail is a byproduct of posting, not a project you start after the letter. Consistent methodology, journal entries written back to the GL with the rationale attached, and a per-line record of who approved what and when: that is the whole capability, and it is exactly what a "somebody writes a paragraph" process cannot fake under examination.

Where does Ceviche fit?

Ceviche is audit-grade expense-allocation software that applies the firm's methodology and writes journal entries back to the GL with the rationale, approver, and date attached to each line, so the audit trail is built as you post rather than reconstructed under exam pressure. Flybridge runs it across 18 fund entities on QuickBooks Online and Bill.com, producing an end-to-end record from invoice to journal entry to underlying expenses. You can see how Ceviche handles fund expense allocation.

FAQ

How common are audit-trail gaps in fund expense allocation? In Ceviche's 2026 analysis of 80 fund finance teams, 49% (39 of 80) have a gap in their allocation audit trail. It is the lowest of the five headline pains in the dataset and skews toward SEC-registered and PE firms, where the cost of not being able to reconstruct an allocation is highest.

What does the SEC look for in expense allocation? Examiners test whether expenses that benefited the adviser were charged to the funds, whether the allocation methodology is documented and applied consistently, and whether each split matches the fund documents. Two of those three are documentation questions, which is why fee and expense allocation stays a recurring priority for the SEC's exam program.

What creates a complete allocation audit trail? A per-line record built as you post, not after: the methodology used for each line, the approver, the date, and the LPA basis that permits the charge. When that record lives in journal entries written back to the GL instead of a spreadsheet, an exam request becomes a minutes-long export rather than a week and a half of reconstruction.