TL;DR. Intercompany accounting records, reconciles, and eliminates transactions between entities under common control, so consolidated financials show no double-counting. Each entity posts its side and the matching balances net to zero in consolidation. For a private fund, the entities are not corporate subsidiaries: they are the management company, the funds, co-invest vehicles, the GP, and SPVs.

What is intercompany accounting?

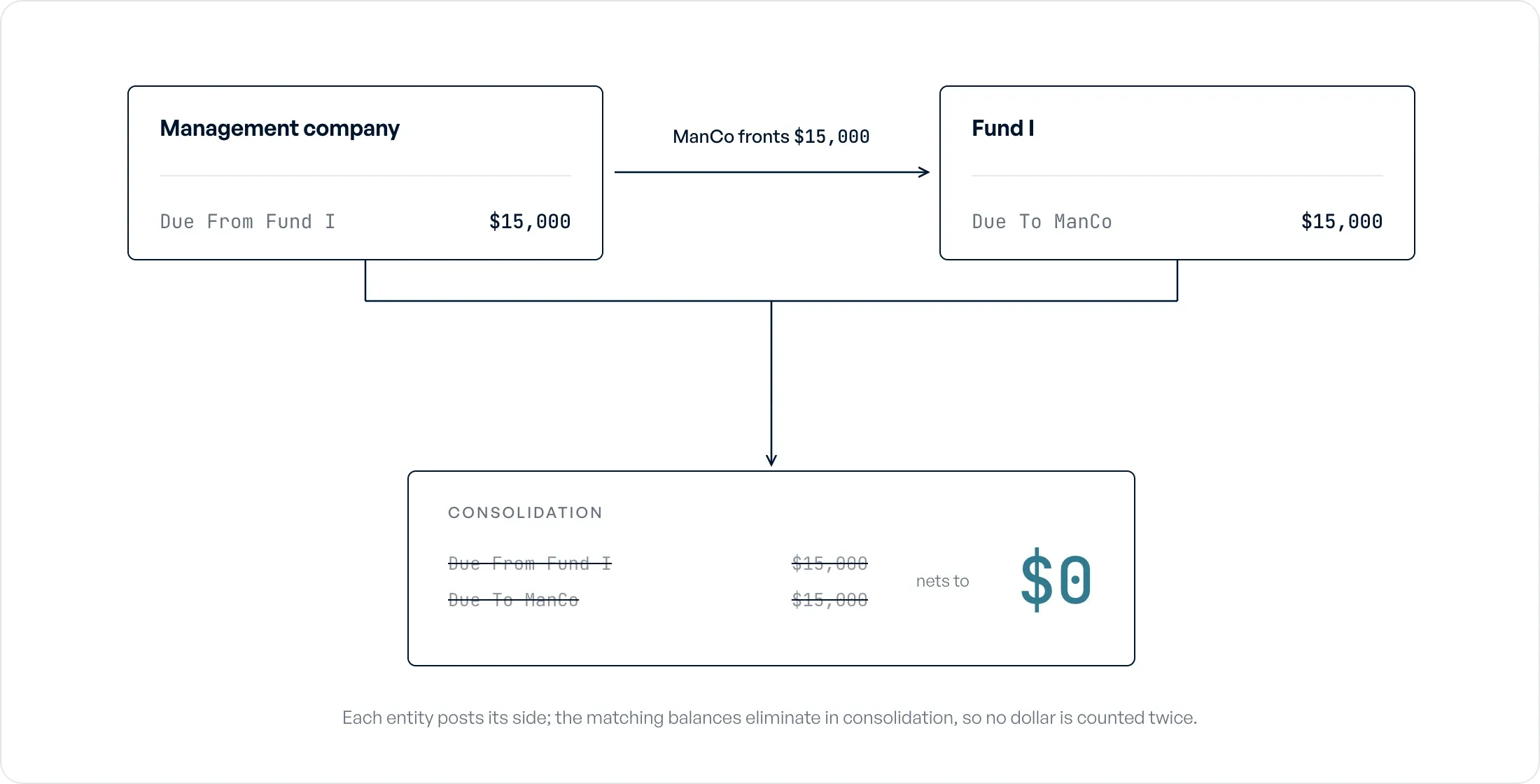

Intercompany accounting records, reconciles, and eliminates the transactions that flow between legal entities owned by the same parent. When two related entities trade with each other, lend to each other, or share a cost, each one posts the transaction on its own books. Those internal transactions are real for each entity but not for the group, so they get removed in consolidation. Otherwise the parent counts the same dollar twice.

For a private fund the principle holds, but the entities change. There is no single corporate parent with subsidiaries beneath it. There is a management company, several funds, a GP entity, co-invest vehicles, and SPVs, all under common control and constantly moving money between one another. A management company fronts a shared bill and the funds owe it back. One fund pays an SPV's formation cost. These are intercompany transactions, and they behave differently than a manufacturer shipping parts to its own factory.

Intercompany accounting is the recording, reconciliation, and elimination of transactions between legal entities under common control. Each entity posts its side of the transaction; matching intercompany balances are reconciled between the entities and then eliminated in consolidation so the parent's financial statements count no internal transaction twice.

Why does intercompany accounting matter?

The point is a consolidated picture that is true. If Fund I books a cost it owes the management company and the management company never books the matching receivable, the group's balance sheet is wrong, and so is every report built on it. Clean intercompany accounting is what lets a parent add up its entities without inflating revenue, expense, or assets.

It also carries the compliance weight. For a private fund, intercompany entries are where an SEC examiner looks to see whether costs landed on the right entity and whether the split matches the fund documents. The SEC's Division of Examinations has named fee and expense allocation a recurring priority for private fund advisers. An entry that nets out cleanly but cannot explain why each line went where it did is a balanced set of books with a hole underneath it.

Intercompany vs. intracompany transactions

These two get used interchangeably and they are not the same. The distinction is the legal-entity boundary.

An intracompany transaction stays inside one legal entity: a transfer between two departments, two cost centers, or two divisions of the same company. There is no second set of books and nothing to eliminate, because the entity is whole. It is internal management reporting, not consolidation.

An intercompany transaction crosses from one legal entity to another under the same parent. Two separate ledgers are involved, each posts its side, the balances have to agree between them, and the pair gets eliminated when the group consolidates. For a fund, almost everything that matters is intercompany: the management company and each fund are distinct legal entities with distinct books, distinct LPs, and distinct LPA rules.

What are the types of intercompany transactions?

Intercompany activity sorts two ways: by direction, and by kind. Direction tells you which entity initiated it relative to the parent.

| Direction | What it means | Fund example |

|---|---|---|

| Downstream | Parent to subsidiary | Management company fronts a fund's expense |

| Upstream | Subsidiary to parent | A fund reimburses the management company |

| Lateral | Between two entities at the same level | One fund covers a co-invest SPV's cost |

By kind, the common categories are shared cost allocations (one entity pays a cost several share, like legal, IT, insurance, or a vendor bill, and bills the others their portion), loans and interest (one entity fronts another working capital, often before a capital call lands), service charges (the management company charges a fund under the LPA), and asset transfers (an asset moves between entities at cost or fair value). Royalties and licensing are common in corporate groups and rare in funds. For most private funds the shared-cost line dominates, and the hardest version of it is a legal invoice.

Intercompany accounting for funds: why fund structures make it harder

Here is the gap every generic guide leaves open. The standard intercompany model assumes a parent and its subsidiaries, where the relationships are stable and the chart of accounts was designed once. A fund group is not that. It splits shared costs across what is often six or more sets of books: the management company, multiple funds, the GP entity, co-invest vehicles, and SPVs, each with its own LPA, its own LPs, and its own rules for what it can be charged.

The data says this is nearly universal. Across 80 PE and VC fund finance teams we interviewed, 96% named multi-entity allocation as a core source of complexity, and 92% ran the work across disconnected systems that do not talk to each other. The management company sits on QuickBooks or NetSuite, the funds sit on a separate fund-side system, and a spreadsheet wedged between them does the actual splitting. Nothing carries a line-level intercompany decision from one system to the next, so a person re-keys it. That re-keying is where intercompany balances drift out of agreement.

A second difference: fund intercompany entries have to survive an LP or SEC exam. A corporate parent eliminating intercompany inventory is doing math. A fund controller posting a due-to / due-from for a fronted legal bill is making a methodology decision per line that an examiner can later question. The structure does not just multiply the entries, it raises the bar on each one.

Intercompany journal entries: due to / due from explained

When one entity pays a cost on behalf of others, you record it with a matched pair of intercompany accounts: due from (a receivable, an asset, debit balance) on the books of the entity that is owed, and due to (a payable, a liability, credit balance) on the books of the entity that owes. One entity's due from is always the counterparty's due to. The full mechanics, including the netting convention and where these accounts live in your chart of accounts, are in the guide on due to / due from in fund accounting.

A worked example. The management company pays a $40,000 shared vendor invoice that benefits Fund I, Fund II, and a co-invest SPV. After applying the allocation methodology the split is Fund I $20,000, Fund II $14,000, SPV $6,000. On the management company's books, it records the receivables it is owed:

| Account | Debit | Credit |

|---|---|---|

| Due From Fund I | $20,000 | |

| Due From Fund II | $14,000 | |

| Due From Co-Invest SPV | $6,000 | |

| Cash | $40,000 |

On each fund's books, that fund records the expense it incurred and the payable it owes. Fund I debits Legal expense $20,000 and credits Due To Management Company $20,000; Fund II and the SPV book the same shape for their amounts. When each fund later wires its share, the due-to and due-from balances clear and the pair returns to zero. That settlement, and the methodology behind each split, is the part that has to hold up later.

Each entity posts its side; the matching balances eliminate in consolidation.

Reconciliation and elimination in consolidation

Intercompany balances live a two-step life. First reconcile, then eliminate.

Reconcile means the two sides agree before you consolidate. The management company's Due From Fund I should equal Fund I's Due To Management Company, to the dollar, every period. They drift apart for ordinary reasons: a timing difference where one entity posts in March and the other in April, an FX move on a cross-currency balance, or a re-key error when the number jumps systems by hand. Reconciliation finds and clears those gaps so the paired balances match.

Eliminate means removing the matched balances when the parent consolidates. Once the two sides agree, the consolidation entry cancels the receivable against the payable, and any intercompany revenue or expense against its mirror, so the group's statements report only what happened with the outside world. Under both US GAAP and IFRS, intragroup balances and transactions are eliminated in full on consolidation, per ASC 810 and IFRS 10.

The catch at fund scale: elimination is only clean if reconciliation was clean, and reconciliation is only clean if the original split was posted consistently on both sides. Funds that allocate in a spreadsheet and post entries by hand routinely find the two sides do not tie at quarter-end, and the close stalls while someone hunts the difference.

The hardest case: allocating a single legal invoice across funds

If you want the sharpest intercompany problem a fund has, it is a legal invoice. In our dataset, 63% of fund finance teams (50 of 80) named legal-invoice allocation one of their hardest problems, the most-flagged single pain after the structural ones.

Here is why it is worse than a normal shared cost. A single outside-counsel invoice can carry dozens of time entries spanning several matters at once: a deal that five funds invested in, a fund's own formation work, a co-invest vehicle's documents, and some management-company corporate housekeeping, all on the same PDF. Each block of lines needs a different methodology. Deal lines split by invested capital across the participating funds, formation lines go to the specific fund that incurred them, and corporate lines stay at the management company. From that one invoice you generate a fan of intercompany entries, each with its own due-to / due-from pair and its own rationale.

Done by hand, this is copy-paste from a billing PDF into a spreadsheet, then re-keyed again into the GL. One controller we interviewed tracked more than 2,800 invoice line items by hand in a single year doing exactly this. The step-by-step version is in the guide on how to allocate legal invoices across fund entities.

What are the challenges of intercompany accounting?

The recurring ones, in roughly the order they bite:

- Matching complexity. The more entities, the more pairs that have to agree. A six-entity fund group has far more intercompany relationships to keep in sync than a parent with two subsidiaries.

- Timing differences. One entity posts its side in one period, the counterparty posts in the next, and the balances disagree until they catch up.

- FX and currency. A cross-currency intercompany balance moves with the exchange rate, so the two sides need a shared convention or they never tie.

- Volume and manual effort. High invoice and line counts, re-keyed across disconnected systems, is where errors enter.

Then the quiet one. 49% of the teams we interviewed (39 of 80) have a gap in their allocation audit trail: the intercompany entry nets out, but the record of why each line went where it did does not survive in a form an examiner would accept. It costs nothing until an audit or an SEC exam, and then it costs a lot. Teams without a trail described their support for a past allocation as "somebody writes a paragraph after the meeting." That is the difference between a balanced set of books and a defensible one. Full data: the audit-trail gap benchmark.

The real cost of manual intercompany accounting is Excel

The competing guides write as if every firm already owns intercompany software. Most fund teams do not. In our 2026 dataset, 81% (65 of 80) still allocated in Excel. The spreadsheet is the real intercompany system in this category: it holds the methodology, it generates the splits, and it is usually maintained by one person with no audit trail behind it.

That has a price, and it shows up at the close. The clearest before-and-after we have: a multi-billion-dollar fund replaced roughly 10 days of manual allocation and reconciliation inside its close with a 1-to-2-hour automated run, taking 5 to 10 days off month-end. No incumbent tool here publishes a close-time benchmark, so that number is, as far as we can tell, the first of its kind. Full data: the fund close-time benchmark.

Best practices for fund intercompany accounting

Less a vendor checklist, more what the teams who have this under control actually do:

- Define the methodology once, then apply it the same way every period. The drift that breaks intercompany balances comes from re-deciding the split each quarter. Set committed-capital, specific-fund, and management-company rules per cost type and stop relitigating them.

- Classify at inception. Decide whether a cost is direct-fund, management-company, or intercompany when it arrives, not at quarter-end when the context is gone.

- Post both sides at once. Generate the due-from and the due-to from the same decision so they cannot disagree. The drift problem is mostly a two-sides-entered-separately problem.

- Settle on a cadence. Carry-forward balances that never clear become a reconciliation backlog. Wire and clear on a schedule.

- Build the audit trail as you post. Every line should already carry its methodology, its approver, and its date. Reconstructing that later is the close's worst fire drill.

What is the R2R intercompany process flow?

Record to report (R2R) is the close cycle that turns transactions into financial statements, and intercompany has a defined place in it: record, reconcile, eliminate.

- Step 1: Record. Each entity posts its side of every intercompany transaction, the due-from on one set of books and the due-to on the other, with the methodology applied per line.

- Step 2: Reconcile. Before consolidating, confirm the paired balances agree across entities, clearing timing, FX, and re-key differences so each due-from equals its matching due-to.

- Step 3: Eliminate. In consolidation, cancel the matched balances and any intercompany revenue or expense against its mirror, so the group's statements report only external activity.

For a fund, this sits inside the month-end or quarter-end close. The teams that move fastest are the ones that recorded consistently and posted both sides together in Step 1, because that is what makes Steps 2 and 3 mechanical instead of investigative.

Where does Ceviche fit?

This is the workflow Ceviche automates after the controller makes the decision. It classifies each expense as direct-fund, management-company, or intercompany, applies the firm's methodology per the LPA, and creates the matched due-to / due-from entries, then writes audit-ready journal entries back to the general ledger with the rationale attached. It sits on top of the systems funds already run rather than replacing them. Flybridge runs it across 18+ fund entities on QuickBooks Online and Bill.com. You can see how Ceviche handles fund expense allocation.

FAQ

What is an example of intercompany accounting? A management company pays a $40,000 shared vendor invoice benefiting two funds and a co-invest SPV. It books a due-from receivable for each entity's portion; each entity books the expense and a due-to payable for its share. When the funds reimburse the management company the balances clear, and in consolidation the receivables and payables eliminate against each other.

What is the journal entry for intercompany? The entity that pays debits a due-from receivable and credits cash. The entity that owes debits the expense (or asset) and credits a due-to payable. One side's due-from always equals the other's due-to. When cash settles the balance you reverse the pair, and on consolidation the two sides eliminate to zero.

What is the R2R intercompany process? R2R is the record-to-report close cycle, and its intercompany steps are record, reconcile, eliminate. Each entity records its side, the paired balances are reconciled so they agree across entities, then the matched balances are eliminated in consolidation so nothing is double-counted in the group financials.

How does intercompany accounting work? Each legal entity under a common parent posts its own side of any transaction with a sibling entity. Those internal balances are reconciled to confirm they match, then eliminated when the parent consolidates, so the group's statements reflect only transactions with the outside world.

What are the steps involved in intercompany accounting? Classify the transaction by entity and type, record both sides with the agreed methodology, reconcile the paired balances each period, settle the cash, then eliminate the matched balances in consolidation. For funds, add one step at the front: decide whether each cost is direct-fund, management-company, or intercompany before you post it.

How does intercompany accounting work for a private fund vs. a corporation? A corporation runs a parent and subsidiaries with stable relationships and one chart of accounts. A fund runs a management company, multiple funds, a GP, co-invest vehicles, and SPVs, each with its own LPA and LPs. The mechanics are the same; the entity count, the per-line methodology decisions, and the LP and SEC scrutiny are higher.

How do you handle intercompany allocation of a legal invoice across funds? Read the invoice line by line, group the time entries by what they relate to, and apply the methodology the LPA supports for each group: invested capital for deal lines, specific-fund for formation work, management company for corporate lines. Then post a due-to / due-from pair per fund with the rationale attached. One invoice usually produces several entries.

What does a defensible intercompany audit trail look like for an SEC exam? Every line traces back to its source invoice, the methodology applied to it, the approver, and the date, built at posting time rather than reconstructed later. An examiner can pull any allocated cost and see why it landed on that entity and that it matched the fund documents. Fee and expense allocation is a standing focus of the SEC's exam program for private fund advisers.