TL;DR. A fund expense is a cost the LPA permits the fund to bear; a management company expense is the cost of running the adviser, paid from the management fee. Decide each line by who benefited and what the fund documents allow, not by which entity the vendor billed. It is one of the least-documented questions in fund finance, and legal invoices are where it bites hardest (63%).

Key findings

- Fund-vs-management-company is one of the least-documented questions in fund finance, addressed mostly in law-firm client alerts rather than any fund-finance data source.

- 63% of fund finance teams (50 of 80) name legal invoices, the hardest fund-vs-ManCo split, among their top pains.

- The split is governed by the LPA, not by which entity the vendor happened to bill.

Methodology

This sub-page draws on Ceviche's analysis of 80 PE, VC, growth-equity, and credit fund finance teams interviewed across 2026: controllers, CFOs, fund accountants, and the fund administrators who serve them. No firm is identifiable in any number here.

Why is the fund-vs-management-company line so hard to draw?

Fund-vs-management-company is one of the least-documented questions in fund finance. The public writing on it is mostly law-firm client alerts and advisory PDFs that never sit in the controller's seat with a real invoice, so the available answers read like legal disclaimers instead of working rules. The question is genuinely hard, for a reason.

The reason the question is hard is that it has two layers. First, who actually benefited from the cost: the funds, the GP, a deal, or the adviser running the shop. Second, what the limited partnership agreement permits the fund to bear. A cost can clearly benefit the funds and still belong to the management company if the LPA does not let the fund carry it. Get either layer wrong and you have either charged LPs for something they should not pay, or eaten a cost the fund was meant to bear. The SEC's Division of Examinations has made fee and expense allocation a standing priority for private fund advisers for exactly this reason: the line is where advisers and LPs have a built-in conflict. On the investor side, ILPA has pushed for clearer disclosure of which costs the fund bears.

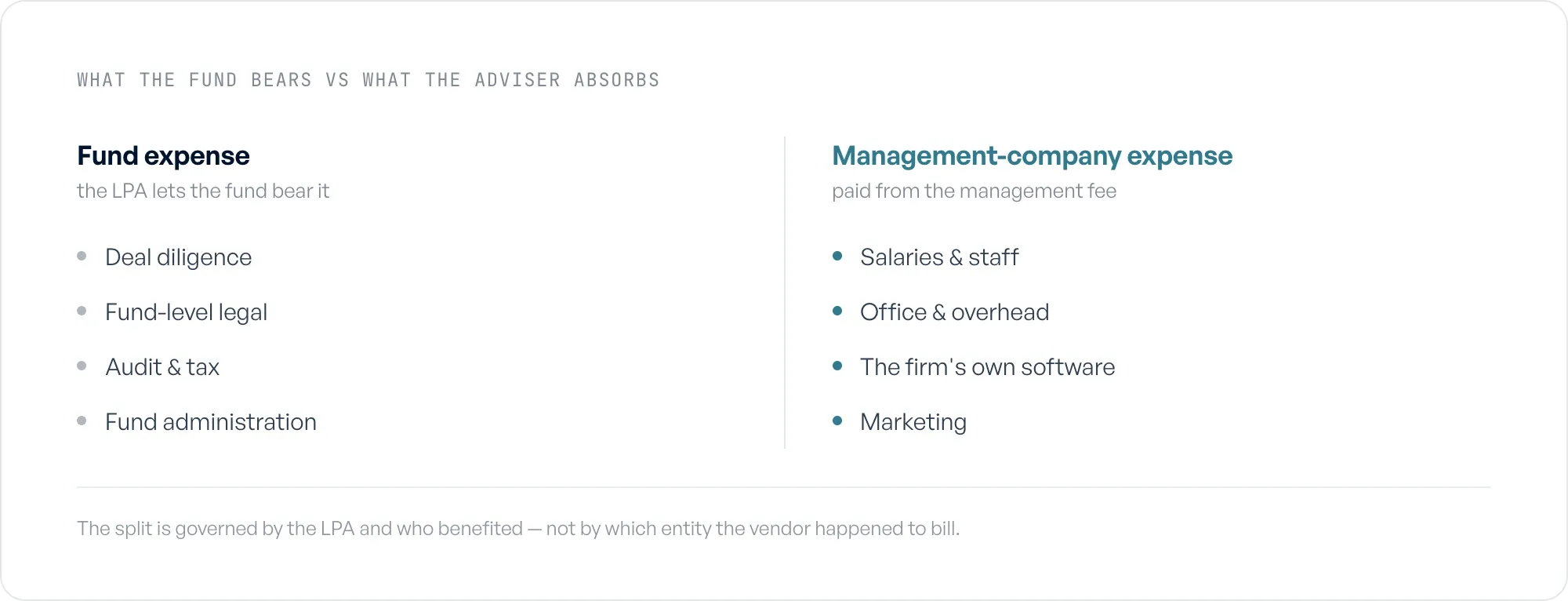

Here is the working definition the data points at. A fund expense is a cost the LPA lets the fund bear, because the fund or its investors benefited and the documents permit it: deal diligence, fund-level legal, audit and tax, administration, and the like. A management company expense is the cost of running the adviser itself, paid out of the management fee: salaries, office, the firm's own software, marketing. The framework that closes this gap is a written methodology applied the same way every time, so two controllers reading the same invoice reach the same split. For the accounting treatment behind these categories, the AICPA's investment-companies guide is the standard reference.

What the fund can bear versus what the adviser absorbs, governed by the LPA.

What makes legal invoices the hardest line to classify?

Legal invoices are where the fund-vs-ManCo question stops being theoretical. 63% of the teams we interviewed (50 of 80) named legal-invoice allocation among their hardest problems, the sharpest single pain in the dataset after the structural ones. A single outside-counsel invoice can carry dozens of time entries: some clearly fund-level, some clearly the adviser's own legal, some that benefited one fund and not another, and a remainder that has to land on the management company. The vendor billed one entity. The right answer splits across several.

A growth-equity controller we interviewed described single invoices that had to split across eight to thirteen funds and SPVs at once, each line read and judged before it could be posted. Another told us they "get one invoice that sometimes gets allocated over like 10 different funds," by hand, every quarter. The classification is the work. Once you know which lines the fund can bear and which the management company absorbs, the arithmetic is trivial; deciding that, defensibly, line by line, is not.

Legal-invoice allocation is also widely mis-categorized, because almost nothing public links splitting a LEDES invoice across fund entities to fund accounting. It is a fund-finance problem wearing a legal-billing costume. Closing this gap requires a consistent methodology per line, journal entries written back to the GL, and an audit trail built as you post, so each split already carries its LPA basis. For the step-by-step workflow, see how to allocate legal invoices across fund entities. For the full benchmark, start at the State of Fund Expense Allocation 2026.

How do firms decide fund vs management company in practice?

The teams that have this under control do not decide invoice by invoice from memory. They set the rule once, at the vendor or GL-account level, against the LPA, and let it run. The pattern we saw repeatedly: encode what each fund can bear, including any caps the LPA sets (a due-diligence ceiling, for instance), then classify every incoming line as fund-level, management-company, or intercompany, and post it the same way every period. One controller, shown this approach, said they had not seen anybody take it; their existing process kept the rules in one person's head and a spreadsheet.

The teams without that discipline pay for it twice. They pay in time at the close, re-deciding the same vendor's invoice each quarter, and they pay in exposure when an examiner asks why a cost went where it did. The honest answer in those shops is often that one person decided and nobody wrote down why. What closes the gap is the same three things every time: a methodology consistent across periods and people, entries written back to the GL rather than re-keyed, and the rationale captured as you post instead of reconstructed under exam pressure. The classification belongs to the controller. Everything after the decision does not have to stay manual.

Where does Ceviche fit?

The judgment of which costs the fund can bear stays with the controller; that is the part the LPA governs and no software should guess. Ceviche is audit-grade expense-allocation software that takes it from there: it applies the firm's allocation methodologies per the LPA, classifies each line as fund-level, management-company, or intercompany, and writes audit-ready journal entries back to the GL with the rationale attached. Flybridge runs it across 18 fund entities on QuickBooks Online and Bill.com. You can see how Ceviche handles fund expense allocation.

FAQ

What expenses can a PE fund charge to the fund vs the management company? A fund can bear costs the LPA permits because the fund or its investors benefited: deal diligence, fund-level legal, audit and tax, and fund administration are typical. The management company absorbs the cost of running the adviser, paid from the management fee: salaries, office, the firm's own software, and marketing. The LPA is the controlling document, and the SEC tests whether the split matches it.

How do firms decide fund vs management company expense? They classify each cost by two tests: who actually benefited, and whether the fund documents allow the fund to bear it. The disciplined teams set that rule once per vendor or GL account against the LPA, then apply it the same way every period rather than re-deciding each invoice, so two people reading the same line reach the same answer.

What does the LPA allow a fund to bear? The limited partnership agreement defines, often in a dedicated expense section, which categories the fund can carry and any caps that apply. Costs that benefited the adviser rather than the fund stay with the management company even when they look fund-related. When a line falls in a gray area, the documented methodology and the LPA basis are what an examiner asks to see.