TL;DR. For a private fund, "fund accounting software" splits into three lanes: nonprofit tools, investment back-office suites, and ERP ledgers. None is the real choice. Across 80 PE and VC finance teams, 81% still allocate in Excel, so the real decision is spreadsheet versus a system that reads your spend tools, applies your methodology, and posts back to your GL.

What does fund accounting software actually do?

Fund accounting keeps money separated by source and restriction instead of pooling it. A nonprofit tracks restricted grants apart from the general fund. A private fund tracks costs and capital by vehicle: Fund I, Fund II, the GP entity, co-invest SPVs, and the management company, each with its own set of books and its own rules for what it can be charged.

Software in this category exists to hold those separate books, post entries to the right one, and produce reporting per entity rather than one consolidated statement. For a private fund that means partnership accounting, multi-entity and multi-fund support from a single instance, investor-ready financials at quarter-end, and an audit trail that ties each entry back to its source. The AICPA's investment-companies guide is the GAAP reference for how these books are kept.

Fund accounting is an accounting method that segregates resources into separate funds by source and restriction, tracking each fund as its own self-balancing set of books. For private funds, each vehicle (a fund, an SPV, the GP, the management company) is a fund, and shared costs must be allocated across them under the rules in the partnership agreement.

That last word, allocation, is where the category gets interesting and where most software stops short. Holding separate books is solved. Deciding how a single shared cost splits across them, and proving the split later, is not.

Three lanes, and why none is the real choice; 81% still run allocation in Excel.

Why isn't generic accounting software like QuickBooks enough?

Most private funds already run a general ledger, and for the management company it is usually QuickBooks or NetSuite. In our data those two cover 73% of management-company GLs, with QuickBooks at roughly half and NetSuite a clear second (the fund finance tech stack). A separate fund-side system (Investran, Allvue, Carta, Geneva) often sits behind that ledger.

So the question is rarely "can QuickBooks do the books." It can. The question is what happens to a shared cost before it reaches the books. A QuickBooks or NetSuite ledger records an entry once you tell it which entity and how much. It does not decide that a $35,000 legal bill splits 60% to Fund II by committed capital, 25% to a co-invest SPV, and 15% to the management company. A person decides that, almost always in a spreadsheet, and then re-keys the result into the GL.

That handoff is the gap. 92% of the teams we interviewed (74 of 80) run their allocations across systems that do not talk to each other: a spend tool on one side, the GL on the other, and a spreadsheet wedged in the middle carrying the actual split. The generic ledger is fine. The allocation layer in front of it is missing.

Which lane of fund accounting software does a private fund need?

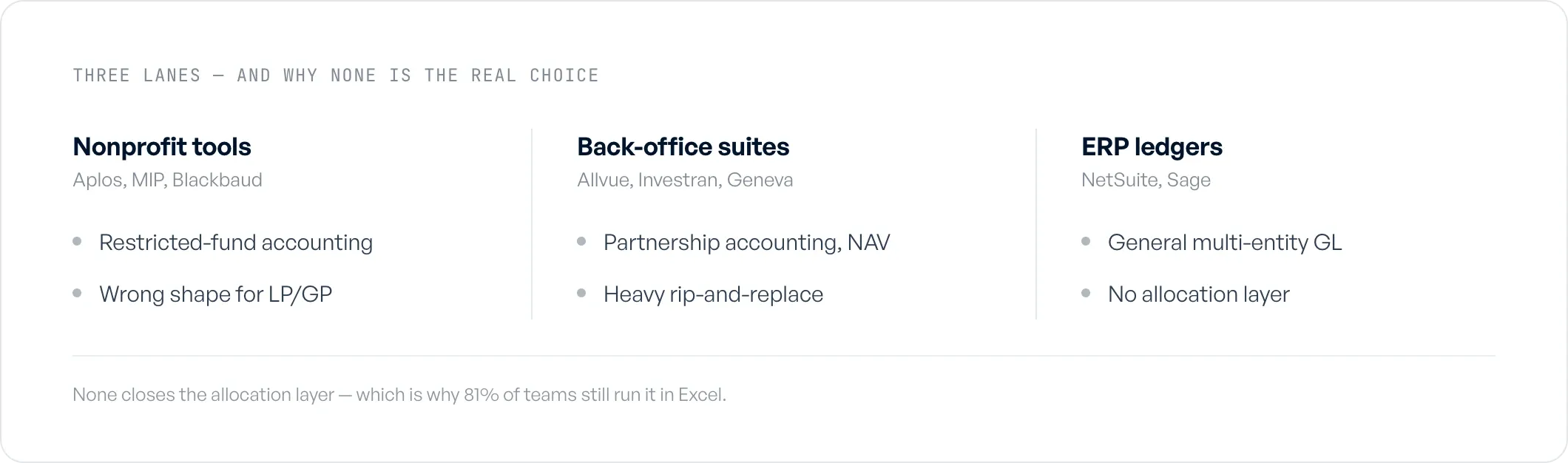

Search "fund accounting software" and you get a mixed bag, because the term covers three audiences. Knowing which lane you are in saves a month of demos.

- Nonprofit and grant accounting (Aplos, MIP, Blackbaud, Sage Intacct for nonprofits). Built around restricted funds, grants, and donor reporting, with FASB and GASB compliance. Excellent for a foundation or a church. Wrong shape for an LP/GP structure.

- Investment back-office suites (Allvue, FIS, Investran, Geneva). Built for fund administrators and large managers: partnership accounting, capital calls, NAV, waterfalls, investor reporting. Powerful and expensive, and a heavy rip-and-replace of your ledger. Aimed more at the fund admin than the controller running a lean team.

- ERP and general ledgers (NetSuite, Sage Intacct, QuickBooks). Where most funds keep the management-company books. Strong on the GL, weak on multi-entity expense allocation, which they treat as a manual journal-entry exercise.

- The allocation layer. The piece almost no one names: software that sits between the spend tools and the GL, decides how each shared cost splits across entities under the LPA, and writes the entries back. This is the layer the spreadsheet currently occupies.

Most private funds in the $500M to $10-15B range do not need a new ledger and cannot justify a back-office suite. They need the allocation layer on top of the ledger they already run.

What do private-fund finance teams actually struggle with?

Every ranking page on this keyword is a vendor describing its own product. None of them tells you what your peers actually run into. We have that data, because we coded 80 PE and VC finance conversations for the same set of pains (the full report).

- 96% cite multi-entity allocation as a core complexity (77 of 80). It is the most universal pain in the dataset, and it scales with entity count, not assets. A firm with three funds, a few SPVs, a GP, and a management company is already splitting shared costs across six or more books every quarter.

- 92% run allocations across disconnected systems (74 of 80). Nothing carries the line-level decision from the spend tool to the GL, so a person does.

- 81% still allocate in Excel (65 of 80). The spreadsheet is the source of truth, maintained by one person, usually with no audit trail. It holds until the entity count climbs or that person leaves.

- 49% have a gap in their allocation audit trail (39 of 80). The split happens; the record of why each line went where it did does not survive in a form an examiner would accept.

One controller summed up the spreadsheet reality plainly: "we just keep a record of everything in Excel, and I'm sure the SEC will love that when they come knocking." That is the buyer you are actually competing with for attention. Not a rival product. A worksheet that has worked so far.

These figures come from the 80 PE, VC, growth-equity, and credit fund finance teams Ceviche interviewed in 2026.

Why is legal-invoice allocation the hardest split?

Of all the splits a fund does, one comes up most: 63% of the teams we interviewed (50 of 80) named legal-invoice allocation one of their hardest problems. A single outside-counsel invoice can carry dozens of time entries spanning several matters, several funds, the GP, co-invest vehicles, and the management company, and each line can need a different methodology.

It is also the most misfiled problem in public information. Almost nothing connects splitting a LEDES invoice (the LEDES e-billing standard) across fund entities to fund accounting, so it gets filed as a legal-billing problem. It is a fund-finance problem wearing a legal-billing costume.

The volume is real. One PE controller tracked more than 2,800 invoice line items by hand in a single year in a spreadsheet, and described single invoices that split across 8 or more funds. When you evaluate software, this is the test case to bring: hand it your worst legal invoice and watch whether it can split one line by committed capital, another by a specific fund, and route the remainder to the management company, with the rationale recorded per line.

How does fund accounting software hold up in an SEC exam?

Allvue says "SOC compliant" and the nonprofit tools say "FASB ready," but compliance of the software is not the same as defensibility of your allocation. The question an examiner asks is whether the split was reasonable, documented, applied consistently, and supported by the fund documents. The SEC's Division of Examinations has named fee and expense allocation a standing priority for private fund advisers.

This is where the audit-trail gap bites. 49% of teams have no record of why a past allocation went the way it did beyond, in one controller's words, "somebody writes a paragraph after the meeting." The teams that stay calm during an exam build the support as they post, so every allocated line already carries its methodology, its approver, and its date before anyone asks (the audit-trail gap benchmark).

When you assess a tool, look past the SOC 2 logo and ask whether the allocation rationale itself is exportable on demand. SOC 2 protects your data. It does not answer the examiner's question.

What does it cost to stay on the spreadsheet?

The cost of manual allocation shows up as time, and it concentrates at the close. Teams reported spending one to five days a quarter on allocation alone, with legal invoices the most time-consuming because every line needs interpretation before it can be split.

The clearest before-and-after in our data: a multi-billion-dollar fund replaced roughly 10 days of manual allocation and reconciliation inside its close with a 1-to-2-hour automated run, taking 5 to 10 days off month-end. No incumbent tool in this category publishes a close-time number, so that figure is, as far as we can tell, the first benchmark of its kind (the fund close-time benchmark). Weigh any software's price against that, not against the sticker on a back-office suite.

How do you choose fund accounting software for a private fund?

Most "how to choose" advice is a feature checklist that every vendor passes. Here is the shorter list that actually separates fit from no-fit for a private fund. Run a tool through these, in order.

- Does it read the spend tools you already run? Ramp appears in roughly half of stacks, with Bill.com and Expensify close behind. If a tool cannot ingest from your AP and card systems, you are still re-keying.

- Does it post back to your existing GL? You should not have to leave QuickBooks, NetSuite, or Sage. A tool that makes you migrate the ledger is solving a problem you do not have.

- Can it apply a different methodology per line, per the LPA? A real legal invoice needs committed capital on one line, a specific fund on another, the management company on the rest. One method for the whole invoice is not enough.

- Does it build the audit trail as you go? Who allocated, when, on what basis, with the source document attached. Reconstructing it later is the exact thing that fails an exam.

- Does it handle your entity count from one instance? Multi-fund, multi-entity, intercompany due-to/due-from generated automatically, not as separate manual entries.

- Is it priced to the work, not to AUM? A $2B fund and a $10B fund can do the same amount of allocation. Pricing on assets penalizes the wrong variable.

If a tool fails 1, 2, or 4, it does not replace your spreadsheet, it adds a fourth system beside it.

Where does Ceviche fit?

Most of allocation is judgment, and judgment stays with the controller. Everything after the decision does not have to stay manual. Ceviche is the allocation layer described in step 1 through 4 above: it sits between the spend tools (Ramp, Bill.com, Expensify, Brex, Concur) and the GL (QuickBooks, NetSuite, Sage), applies the firm's methodologies per the LPA, and writes audit-ready journal entries back. It is not an ERP, not a fund admin, and not a service that does the allocations for you. Flybridge runs it across 18 fund entities on QuickBooks Online and Bill.com, went from a full day of spreadsheet allocation each quarter to a hands-off run at about 99% accuracy, and onboarded in two weeks. You can see how Ceviche handles fund expense allocation.

FAQ

Can QuickBooks handle fund accounting? QuickBooks runs the management-company general ledger for about half the private funds in our 2026 data, and it handles the books well. What it does not do is decide how a shared cost splits across fund entities. That allocation happens upstream, almost always in a spreadsheet, and the result is re-keyed into QuickBooks. So QuickBooks handles the ledger, not the multi-entity allocation in front of it.

What is a fund accounting system? A fund accounting system keeps money in separate, self-balancing funds rather than one pool, posting each transaction to the fund it belongs to and reporting per fund. For a private fund, each vehicle (a fund, an SPV, the GP, the management company) is a fund, and the system has to allocate shared costs across them under the rules in the partnership agreement.

What software do most CPAs use? For private-fund clients, CPAs and controllers work in whatever ledger the firm runs, and in our 2026 dataset that is QuickBooks for roughly half and NetSuite for a clear second, together 73% of management-company GLs. The fund-side accounting often sits in Investran, Allvue, Carta, or Geneva behind that ledger. The shared-cost allocation between them still tends to live in Excel.

What are the 5 fund accounting software options for private funds? Five names a private fund actually encounters: NetSuite and QuickBooks for the management-company ledger, Investran and Allvue for fund-administration back-office work, and Excel, which 81% of teams still use for the allocation itself. The gap that none of those five closes well is the allocation layer between the spend tools and the GL.

What is the best fund accounting software for private equity? There is no single best, because the lanes serve different jobs. For partnership accounting and NAV at a fund admin, the back-office suites fit. For the management-company GL, QuickBooks or NetSuite. The piece most PE controllers are missing is not a new ledger, it is the allocation layer that splits shared costs across entities and posts back to the ledger they already run.

Do you need fund accounting software, or is Excel enough? Excel is enough until it is not, and 81% of the teams we interviewed are still on it. The line is entity count and exam exposure: once shared costs split across six or more vehicles, or once an examiner asks why a past allocation went the way it did, a spreadsheet with no audit trail becomes the risk. At that point the choice is not which spreadsheet, it is a system that records the methodology and the rationale as you post.