TL;DR. Fund accounting tracks money in separate, self-balancing pools called funds, with each fund accountable for how its money is raised and spent rather than for turning a profit. Nonprofits, governments, and private investment funds all use it. At a private fund, the daily reality is allocating shared costs correctly across many entities.

What is fund accounting?

Fund accounting is a method of tracking money in distinct pools, called funds, where each pool is a self-balancing set of books with its own assets, liabilities, and rules for how the money can be used. The point is accountability, not profitability. Instead of asking "did the organization make money," fund accounting asks "did each fund's money get raised and spent the way it was supposed to."

That second question is why the method exists. A donor restricts a gift to scholarships. An LP commits capital to Fund III and not to the management company. In each case someone outside the organization put a fence around the money, and the books have to honor that fence. Regular accounting rolls everything into one set of statements. Fund accounting keeps the fences standing.

Who uses fund accounting?

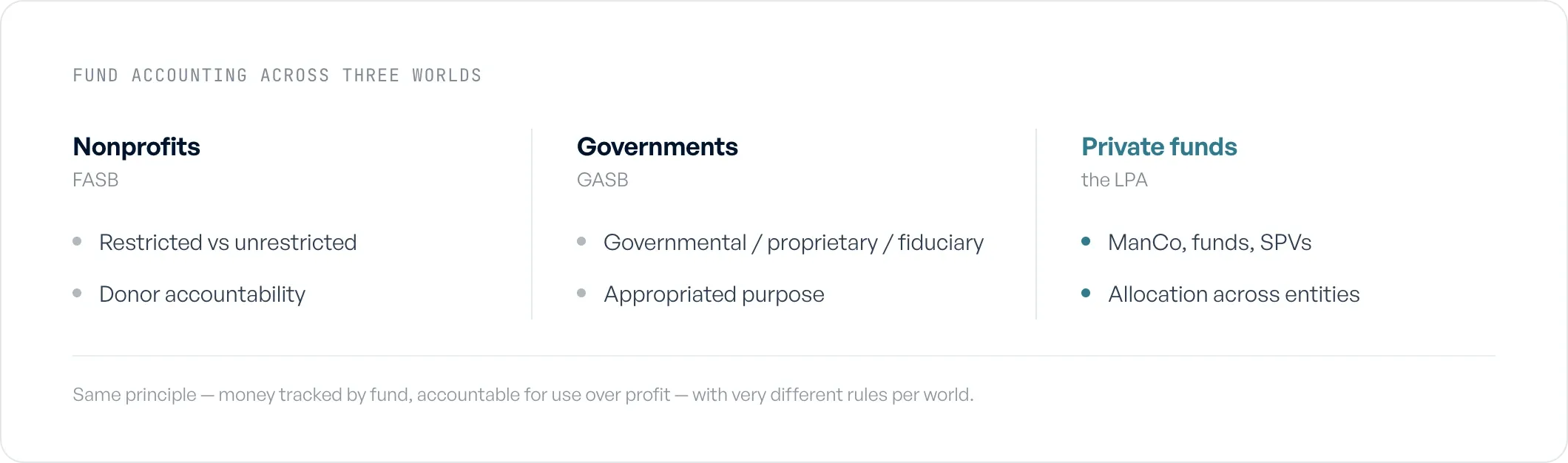

Three kinds of organizations rely on it, and most guides put them in the wrong order for our reader.

Private investment funds. PE, VC, growth-equity, and credit funds run a management company, one or more funds, a GP entity, and often a stack of SPVs and co-invest vehicles. Each is its own set of books. Shared costs, legal, travel, technology, due diligence, get split across them according to what the limited partnership agreement allows. This is fund accounting at its most granular, and the version almost nobody explains.

Nonprofits. Charities, foundations, and universities track donor-restricted and unrestricted funds separately so a restricted gift never quietly subsidizes general operations. This is the framing most search results lead with, because it is where the term first took hold.

Governments. Federal, state, and local bodies use fund types (governmental, proprietary, fiduciary) to keep tax dollars tied to their appropriated purpose. The Governmental Accounting Standards Board sets the rules here, separate from the standards a business follows.

The common thread is restriction. Whenever money carries a string from a donor, a regulator, or an investor, fund accounting keeps that string attached.

Fund accounting across three worlds.

How is fund accounting different from regular accounting?

Regular, for-profit accounting measures one thing well: whether the business made money. Everything funnels into a single income statement and balance sheet, and the scorecard is net income. Fund accounting measures whether each pool of money stayed inside its boundaries. There can be a dozen self-balancing sets of books under one roof, and "profit" may not be the question for any of them.

| Regular (for-profit) accounting | Fund accounting | |

|---|---|---|

| Core question | Did we make a profit? | Did each fund's money stay within its restrictions? |

| Books | One consolidated set | Multiple self-balancing funds |

| Headline metric | Net income | Accountability and compliance per fund |

| Who sets the boundary | Management | Donors, regulators, LP agreements |

| Typical users | Operating companies | Nonprofits, governments, private funds |

For a private fund the contrast is sharper than the table suggests. A single travel expense might belong half to Fund I, a quarter to Fund II, and the rest to the management company. In for-profit books that is one line in one ledger. In fund accounting it is one decision that has to land correctly in three sets of books and reconcile between them.

What are the building blocks: funds, entities, and restrictions?

A fund is the basic unit, and a restriction is what makes it a fund rather than a bucket. The building blocks differ by who you are. Nonprofits split funds into restricted versus unrestricted: money a donor fenced off versus money the organization can spend freely. Governments use governmental, proprietary, and fiduciary fund types. At a private fund, those building blocks are entities:

- The management company (ManCo), which runs the firm and bears the operating costs the LPs do not pay for.

- The funds, each governed by its own LPA that dictates what can and cannot be charged to it.

- SPVs and co-invest vehicles, single-purpose entities that hold a deal or let specific investors participate alongside a fund.

Every shared cost has to find its correct home among these, and the LPA is the rulebook. The recurring definitional question, what can a fund be charged versus the management company, has almost no clear answer published anywhere. We covered it in fund expenses vs management company expenses.

Fund expense vs management company expense. A fund expense is a cost the limited partnership agreement permits charging to the fund, deal legal fees or fund audit costs, for example. A management company expense is an operating cost the firm bears itself, like salaries or office rent. Miscategorizing the two is the error SEC examiners look for.

What does fund accounting actually look like inside a private fund?

Here is where the standard definition stops being useful. Inside a private fund, fund accounting is not mostly bookkeeping. It is mostly allocation: taking one shared cost, dividing it correctly across many entities, posting the result to each ledger, and reconciling between them. Our own research shows how dominant this is.

Across 80 fund finance teams Ceviche spoke with in 2026, 96% named multi-entity allocation as a core source of complexity, and 92% were running that work across systems that do not talk to each other. Structure, not asset size, drives the difficulty. A firm with three funds, a couple of SPVs, a GP, and a management company is already maintaining six or more sets of books that each need their slice of every shared bill.

And most of that work still happens in a spreadsheet. 81% of those teams were allocating expenses in Excel in 2026. The spreadsheet is the source of truth, one person maintains it, and it usually carries no record of who decided what. It holds up until the entity count climbs or that person leaves. One controller we interviewed for the research put it plainly: "we just keep a record of everything in Excel, and I'm sure the SEC will love that when they come knocking." The full breakdown is in our state of fund expense allocation report, with the structural detail in the multi-entity allocation benchmark.

Why is legal-invoice allocation the hard part, and where does the audit trail break?

Ask fund controllers which cost is hardest to allocate and one answer comes back more than any other. 63% of the teams in our 2026 research named legal-invoice allocation among their hardest problems. A single outside-counsel invoice can carry dozens of time entries spanning several matters, several funds, the GP, co-invest vehicles, and the management company, and each line can need a different methodology. A growth-equity controller we interviewed described single invoices that split across eight to thirteen funds and SPVs at once, every time, by hand. Read the numbers in the legal-invoice allocation benchmark.

The second hard part shows up later, at audit or SEC exam. 49% of those teams had a gap in their allocation audit trail: the split gets made, but the record of why each line went where it did does not survive in a form an examiner would accept. Fee and expense allocation is a standing focus of the SEC's Division of Examinations for private fund advisers, and the question they press is whether the methodology is documented and applied consistently. A team without a trail described its support for a past allocation as "somebody writes a paragraph after the meeting." Details are in the audit-trail gap benchmark.

The payoff for fixing both is concrete. One multi-billion-dollar fund cut its month-end allocation work from roughly ten days of manual reconciliation to a one-to-two-hour automated run, taking five to ten days off close. That came from making the allocation logic consistent and writing the entries and audit trail back automatically, not from working faster by hand.

What does a fund accountant do?

A fund accountant keeps each fund's books accurate, compliant, and reconciled. The role centers on calculating net asset value, recording capital calls and distributions, applying the LPA's rules to every shared cost, and producing the reports LPs and auditors rely on. Equity-method accounting for portfolio holdings and the distribution waterfall, who gets paid in what order when money comes back, sit on that desk too. In practice, much of the week is the allocation work above: deciding how a legal invoice splits, posting the intercompany due-to and due-from entries that keep the funds square, and staying ready to defend each decision later. Some firms keep this in-house; others lean on a fund administrator while their own team owns the harder judgment calls. For the underlying standards, the AICPA's investment-companies guide is the audit and accounting reference auditors work from.

What are the best practices for fund accounting?

The fundamentals apply whether you run a foundation or a credit fund:

- Keep each fund genuinely separate. Self-balancing books per entity, not one ledger with memo tags.

- Write the methodology down before you need it. Document how each category of shared cost gets split against the LPA, and apply it the same way every period.

- Build the audit trail as you post, not after. Every allocated line should already carry its basis, its approver, and its date.

- Reconcile intercompany every close. Due-to and due-from balances between funds should net to zero and be checked, not assumed.

- Use systems that already fit your stack. A new tool earns its place by reading the GL and spend tools you run, not by forcing a migration.

The thread through all five is consistency. Most allocation pain is not a math problem; it is the same decision drifting a little each quarter until nobody can explain the pattern to an auditor.

What software do funds use for fund accounting?

There is little public data on what private funds actually run, so here is ours. Among the teams in our 2026 research, QuickBooks and NetSuite together serve about 73% of management-company general ledgers, usually with a separate fund-side system (Investran, Allvue, Carta) behind them. On the spend side, Ramp, Bill.com, and Expensify dominate. The full distribution is in the fund finance tech stack.

Read that distribution the right way and the implication is clear. The work is rarely about moving a fund onto a new ledger. It is about bridging the management-company GL the firm already runs and the fund-side system behind it, so a shared cost can be allocated once and land correctly in both.

Where does Ceviche fit?

Ceviche is audit-grade expense-allocation software that sits between the spend systems funds already use (Ramp, Bill.com, Expensify) and the general ledger (QuickBooks, NetSuite, Sage), applies the firm's allocation methodologies per the LPA, and writes audit-ready journal entries back with the rationale attached. Flybridge runs it across 18 fund entities on QuickBooks Online and Bill.com, and went from a full day of spreadsheet allocation each quarter to a hands-off run. Ceviche has completed its SOC 2 Type 2 audit. See how Ceviche handles fund expense allocation.

FAQ

What is fund accounting in simple words? Fund accounting tracks money in separate pools called funds, each its own self-balancing set of books with its own rules. The goal is to prove each fund's money was raised and spent the way it was supposed to be, rather than to measure overall profit.

How is fund accounting different from regular accounting? Regular accounting consolidates everything into one set of books and measures profit. Fund accounting keeps multiple funds separate and measures whether each stayed inside its restrictions. For a private fund, one shared cost can split across several entities, each with its own ledger and LPA rules.

What does a fund accountant do? A fund accountant keeps each fund's books accurate and compliant: calculating NAV, recording capital calls and distributions, allocating shared costs per the LPA, posting intercompany entries, and producing LP and audit reports. At private funds, much of that is splitting shared expenses across funds, SPVs, and the management company.

What are the three types of fund accounting? In government, the three fund types are governmental, proprietary, and fiduciary, each with its own reporting treatment per GASB. Nonprofits split funds into restricted and unrestricted. Private funds work at the entity level: management company, funds, and SPVs or co-invest vehicles.

What is fund accounting in private equity? It covers NAV calculation, capital activity, the distribution waterfall, equity-method accounting for portfolio holdings, and allocating shared costs across the funds, SPVs, and management company per each LPA. The allocation piece, especially legal invoices, is where most of the manual time goes.

What is fund accounting with an example? A fund gets one outside-counsel invoice for a deal it pursued across two funds and a co-invest SPV. The fund accountant splits the deal lines by committed capital, charges the formation lines to the specific fund that used them, and posts the result to each ledger with the methodology documented. Repeated across every shared cost, that is fund accounting in practice.

What is fund accounting in investment banking? The term applies to the asset-management and fund side, not the deal-advisory side of a bank. Where a bank runs or administers investment funds, the same discipline applies: separate self-balancing books per fund, NAV calculation, and allocation of shared costs across vehicles.